In recent years, various new payment types triggered by digital innovation have emerged one after another. In human history, consumers have more payment options than ever before.

"In 2023, digital wallet will still be the preferred payment method for consumers, with a total consumption of 14 trillion dollars in all channels." The global payment solution company Worldpay recently released the 2024 Global Payment Report (hereinafter referred to as the "Report"), which shows that digital wallet has become the main payment option for consumers. In 2023, digital wallets will account for 50% of global e-commerce consumption and 30% of global point of sale consumption. In the future, digital wallet will still be the fastest growing payment method.

In addition, among the emerging global payment methods, account to account payment (A2A) and buy before pay (BNPL) also show considerable development potential, and the global payment pattern is still changing.

Strong growth of digital wallet in the world

The report shows that in 2023, it will account for 50% of global e-commerce transactions. Digital wallet is the fastest growing e-commerce payment mode, and the compound annual growth rate is expected to be 15% by 2027. The report predicts that by 2027, the amount of transactions directly paid by credit cards and debit cards in e-commerce transactions will decline slightly. However, this "decline" is largely because the direct consumption expenditure of bank cards has become the consumption expenditure of digital wallets.

At the point of sale, in 2023, the digital wallet will further expand its leading edge in the global point of sale, accounting for about 30% of the global point of sale transaction volume, more than $10.8 trillion. At the same time, digital wallet is also the fastest growing payment method at the point of sale. It is estimated that by 2027, its compound annual growth rate will be as high as 16%.

In the global payment market, China is the world's largest digital wallet market. The three major payment brands, Alipay, WeChat payment and UnionPay, the bank card organization, lead the Chinese payment market.

The above report shows that in 2023, digital wallets will account for 82% of e-commerce transactions and nearly two-thirds (66%) of point of sale consumption. More importantly, digital wallet is still the fastest growing mode of payment, even though it has gained a leading position in e-commerce and point of sale in China. In the e-commerce market, it is expected that the compound annual growth rate of digital wallet will reach 13% from 2023 to 2027, accounting for 86% of the total consumption.

In contrast, American consumers will still favor credit cards to a large extent in 2023. However, digital wallets will also become the fastest growing online and offline payment method in the United States in the future.

The above report shows that according to the existing data, the credit card, debit card and prepaid card in the United States will account for 71% of the total consumption in 2023. The report predicts that in 2027, the proportion of digital wallet transactions in U.S. e-commerce payments will reach 52%, and the proportion of transactions at the point of sale will drop to 31%. Compared with this, the proportion of credit card transactions in the above two channels will decline to 22% and 34% respectively.

It is different from the US market. The report shows that digital wallets lead the European e-commerce payment market, especially in Denmark, Germany, Italy, Spain and the United Kingdom. Amazon Pay, Apple Pay, Google Wallet and PayPal, the global digital wallet brands, are the main participants in European digital payment.

The report predicts that in the European market, digital wallets will account for 30% of e-commerce transactions in 2023, and its compound annual growth rate is expected to reach 17% by 2027, when digital wallets will account for 40% of e-commerce transactions.

In Europe, digital wallets are becoming more and more popular. The report shows that bank cards have dominated the European payment market for decades, and the bank card system is mature and stable, which has become a resistance to change. However, as more businesses are willing to accept digital wallets and more and more consumers use this convenient payment method, the popularity of digital wallets is accelerating. It is predicted that by 2027, the utilization rate of digital wallet at the point of sale will grow at a compound annual growth rate of 24%, accounting for more than double from 13% in 2023 to 27% in 2027.

Bank cards still have a strong influence

People often ask such a question: the market share of bank cards is being swallowed up by digital wallets, and whether the influence of bank cards has declined as a result?

For such a question, the answer given in the above report is no. According to the above report, among global payment methods, with the transfer of market share to digital wallet, bank cards still perform strongly. This is because it seems that the consumption of bank cards is decreasing, but in fact it is just changing into a new digital wallet, or paying by "direct payment" or "installment". Worldpay found in the survey that the main source of funds for consumers' digital wallets is still the combination of credit cards and debit cards embedded in digital wallets, which is not fundamentally different from the situation of using physical cards instead of digital wallets.

The report predicts that bank cards are expected to remain influential for many years in the future and still dominate many markets.

Although bank cards currently occupy a high market share in the payment market, the United States is also carrying out innovation in the financial infrastructure of the real-time payment system. Last July, the Federal Reserve launched the instant payment system "FedNow" to support the modernization of the US payment system. All major banks and credit cooperatives can register and use this tool.

However, this real-time payment system needs time to deposit. According to the above report, it may take several years for FedNow to really affect consumers. The process of banks adopting the new real-time payment service of the Federal Reserve is not smooth. They are still trying to meet the challenges faced by real-time payment, such as how to reduce fraud.

Emerging payment methods cannot be ignored

In addition, among the emerging global payment methods, account to account (A2A) payment and buy before pay (BNPL) have shown considerable development potential.

It is understood that account to account (A2A) payment is an electronic payment made directly from one party to the other without using the card set network. A2A has been embedded in various applications and online services, such as Pix in Brazil, iDEAL in the Netherlands, and BLIK in Poland. A2A payment includes bank transfer (initiating payment) and direct debit (direct deduction).

The report shows that in 2023, in some European countries such as the Netherlands, Malaysia, Thailand and Nigeria, account to account payment will account for at least 30% of the transaction volume in the e-commerce market.

E-commerce payment mode in Europe

Under the influence of the EU's joint supervision, the payment pattern of European e-commerce is very diversified. The report shows that in the European market investigated by Worldpay, credit card, debit card, account to account (A2A) payment and digital wallet are at least in the leading positions in two markets respectively.

Although, as mentioned earlier, digital wallets also lead the European e-commerce payment market in the European market, in terms of emerging payment innovation, this region shows a diversity of characteristics, and various payment methods may be successful. It is difficult for a certain payment method to monopolize the market.

For example, in terms of emerging payment methods, account to account (A2A) payment will lead Finland, the Netherlands, Norway, Poland and Sweden in 2023. A2A payment is particularly prominent in the Netherlands and Poland. In 2023, A2A payment will account for 18% of European e-commerce transactions.

Taking Sweden as an example, the report shows that account to account (A2A) payment will become the preferred online payment method in 2023, accounting for 30% of e-commerce transaction volume, driven by Swedish domestic banking service; Buy first and pay later (BNPL) has won the favor of Swedish consumers. As the hometown of Klarna, the leader of the global buy before pay (BNPL), Sweden's buy before pay (BNPL) will account for 21% of e-commerce transaction volume in 2023, with the highest utilization rate in the world (the same as Germany).

In Latin America, the penetration rate of A2A payment in Latin America will be the highest in the world in 2023, accounting for 20% of the regional e-commerce transaction volume. The great success of Brazil's real-time payment system Pix has promoted the rise of online account to account (A2A) payment in Latin America. In 2023, A2A payment will become the second most popular online payment method in Brazil, accounting for 30% of the transaction volume and ranking first in the region.

However, the report also points out that due to the slow progress in the promotion of the Open Bank Agreement so far and the need for reassessment and revision, A2A payment is expected to grow slowly, accounting for only 19% by 2027. At the same time, account to account (A2A) payment still faces challenges in the market dominated by bank cards.

Compared with digital wallets, credit cards and A2A payments, the proportion of buy before pay transactions in the world is relatively low, accounting for about 5% of global e-commerce transactions in 2023.

"Buying before paying is actually a popular concept in recent years, because it can give payment to ordinary consumers like a credit product. These consumers may not be able to get the credit card limit at the bank end, but they can be given a certain limit after buying and then paying, so that they can use it and stimulate their consumption, because they are provided with more payment options. " Shi Nanfei, general manager of Worldpay China, said that "pay after buy" can be understood as a payment credit product, but it will be subject to very strong supervision by the financial supervision department.

In China, mainstream brands in the buy before pay model include Ant Flower, JD Baitiao, etc. According to the report, pay after buy is expected to further grow in China's e-commerce market. By 2027, the proportion of its transaction volume (5%) may exceed that of direct use of credit cards (4%) and debit cards (3%).

"The rise of emerging payment has a wide range of manifestations, and mobile payment is the most important feature. It not only attracts extensive social attention, but also has a profound impact on people's daily life and work, and has caused a greater impact on traditional payment methods, so that banking financial institutions compete for reform and transformation." The report concluded.

Cash transactions are shrinking but still attractive

From the perspective of cash transaction amount and market share, there is no doubt that cash transactions will shrink in the next few years.

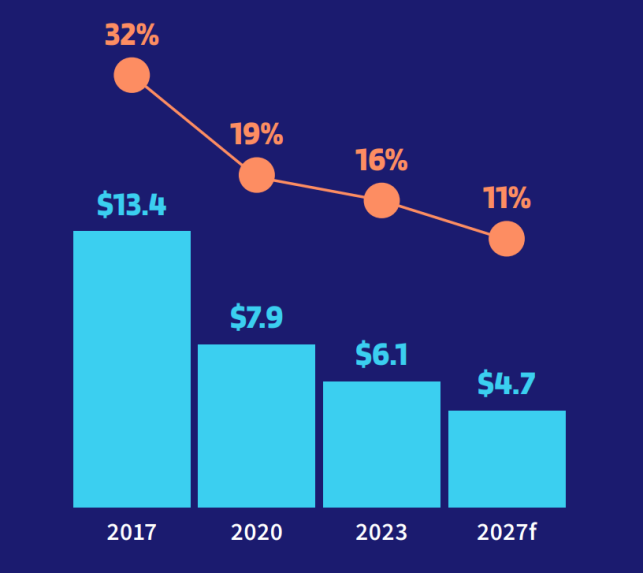

The report shows that globally, the cash transaction volume decreased from 6.7 trillion US dollars in 2022 to 6.1 trillion US dollars in 2023, a year-on-year decrease of 8%. Moreover, the report also predicts that by 2027, the compound annual growth rate of global cash transactions will remain at - 6%, and the cash transactions at global outlets will be $4.7 trillion, accounting for 11% from 16% in 2023.

2017-2027 (forecast) global cash transaction volume/in US $1 billion (percentage of point of sale)

2017-2027 (forecast) global cash transaction volume/in US $1 billion (percentage of point of sale) In 2023, in 12 of the 40 markets surveyed in the above report, the main payment method for point of sale transactions is still cash, such as Argentina, Colombia, Japan and other countries and regions. Correspondingly, in Australia, Canada, China, Denmark, Finland, the Netherlands, New Zealand, Norway, Sweden and other countries and regions, the proportion of cash transactions at the point of sale is less than 10%.

However, cash, with its multiple forms and diversity, is still an important payment tool for billions of consumers around the world. The report shows that in many markets, consumers with lower income prefer to use cash for transactions because they can't get banking services or can only get a small amount of banking services. Cash remains attractive in the face of economic uncertainty.

Editor in charge: Yang Yucheng

When the stock market recovers, open an account first! Intelligent fixed investment, condition sheet, individual stock radar... for you>>

Massive information, accurate interpretation, all in Sina Finance APP

Editor in charge: Yang Ci