[The first Hong Kong Stock Golden Lion Awards were voted by 1000 listed companies] Lei Jun, Ma Mingzhe, Wang Xing and other well-known entrepreneurs competed fiercely. Who will stand out? Xiaomi, Meituan, Bank of China, Galaxy Entertainment, BYD and other star enterprises compete for beauty. Who will be superior to Qunfang? The best Hong Kong stock company of the year is waiting for you to choose! 【 Click to vote 】

Abstract: Has the real estate industry really entered the severe winter? Is it true that the real estate enterprises have ushered in the situation of "the remnant is the king"? Sina Finance combs the main business data of listed real estate enterprises, takes you to see the differences and responses of leading real estate enterprises in "winter", and explores the changes of the industry from financing, land acquisition, sales, local reserves, debt repayment, profits.

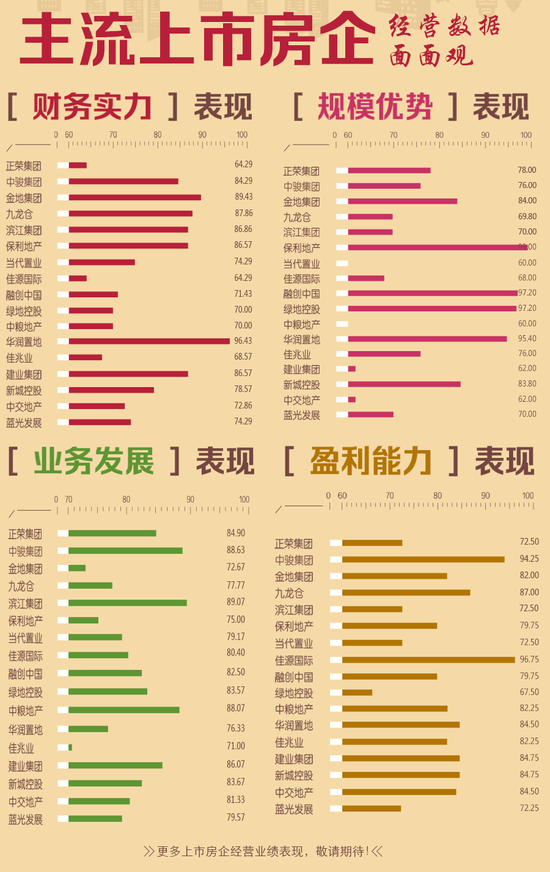

Sorting out of Sina Finance in this issue COFCO Property This year's business performance is compared with the data of the same period last year and the average value of the operating data of 50 mainstream listed real estate enterprises. Meanwhile, Sina Finance classifies the operating indicators and gives them corresponding weights according to the overall business model and operating process of real estate enterprises' development business, referring to the mainstream rating system, to find out the "changes" of COFCO Real Estate since this year from four aspects And "Focus".

In terms of scoring, COFCO Real Estate scored well in terms of business development and profitability, while its scale advantage and financial strength were average.

In terms of business development, COFCO Real Estate acquired land of 3.37 billion yuan in the first half of 2018, which is significantly lower than the average value of the data of mainstream real estate enterprises. In the first half of 2018, COFCO Real Estate's land acquisition area was 1224200 ㎡, significantly slowing down, compared with 349.58 ㎡ in 2017. The sales volume of COFCO Real Estate in the first half of the year was 20.32 billion yuan, and the sales area was 690000 m2. The sales area in the first half of the year increased by 82.44% year on year. In 2017, the sales area of COFCO Real Estate in the whole year was 1322000 m2. The company's inventory turnover rate is slow, but the ratio of sales price to land acquisition price is significantly higher than the average value of mainstream real estate enterprises.

Revenue reserve multiple is a coefficient to evaluate the future performance guarantee strength of a real estate enterprise. COFCO Real Estate's revenue reserve multiple was 39.94 (referring to the half year revenue of 2018), higher than the average value of mainstream real estate enterprise data, while this value was 19.5 in 2017 (referring to the full year revenue of 2017).

In terms of finance, the average financing cost of COFCO Real Estate in the middle of this year was 5.5% lower than that in 2017, lower than the average 6.07% of the average financing cost of mainstream listed real estate enterprises. Data in 2017 showed that the average financing cost of COFCO Real Estate was 6.20%. The net debt ratio was 183%, significantly higher than that in 2017, and significantly higher than the industry average of 125%.

At present, COFCO Real Estate has 9.9 billion yuan of monetary funds+restricted funds, 12.7 billion yuan of short-term debt and 19.8 billion yuan of long-term debt. The short-term debt repayment pressure index is used to assess the debt pressure of a real estate enterprise within a year. The short-term debt repayment pressure index of COFCO Real Estate is 1.27, which highlights the debt repayment pressure and is significantly higher than the average value of the data of mainstream real estate enterprises.

In terms of scale and profitability, COFCO Real Estate has obvious scale advantages, but its profitability scores are not poor. In the first half of 2018, the value of COFCO Real Estate land reserves was 175.9 billion yuan, significantly lower than the industry average of 590.874 billion yuan, and the value of equity land reserves was 107.3 billion yuan, accounting for 61% of equity. COFCO Real Estate's advance receipts (contractual liabilities) were 23.5 billion yuan, lower than the average of the data of mainstream real estate enterprises.

COFCO Real Estate's gross profit rate and net profit rate of sales are higher than the average level of mainstream real estate enterprises. The ROE for half a year is 9.03%, which is also ahead of the industry average.

The performance chart of COFCO Real Estate is as follows:

explain:

(1) The data used for index statistics are all from China Index Research Institute, Kerry, wind data, announcements, public information, etc.

(2) The corresponding indicator measurement score is selected by Sina Finance within a certain period, and the public operating data is given corresponding

Weight, and calculate the score by referring to the mainstream rating system.

(3) The average value of the data of listed real estate enterprises is the arithmetic average of the data of 50 mainstream listed real estate enterprises selected by Sina Finance according to the relevant evaluation system within a certain period.

(4) The operating data of listed real estate enterprises are calculated in the half year of 2018, and some indicators are measured data. Sina Finance calculates them by formula based on public data and corresponding accounting standards.

Sina Finance's [Real Estate Enterprise Atlas] column:

[Real estate enterprise atlas] General net debt ratio of Jiazhaoye's financial strength score reaches 258%

[Real estate enterprise atlas] The financing cost of Jianye Real Estate is up to 7.5%, and the land acquisition is slowing down

[Real estate enterprise atlas] China Resources Land's land acquisition efforts increased without reducing financial pressure

[Real estate enterprise atlas] The increase of financing cost of Blu ray Development has a general profitability score

[Real estate enterprise atlas] CCCC Real Estate's scale score is nearly 10 billion in general short-term and long-term debt

[Real estate enterprise atlas] The land acquisition of New Town Holdings has significantly increased without reducing the net debt ratio

[Real estate enterprise atlas] Binjiang Group's financing cost rise, scale and profit score are average

[Real estate enterprise atlas] Jiulongcang: sales area declines, short-term debt repayment pressure is high

[Real estate enterprise atlas] The business development score of Jindi Group's long-term debt of 57.5 billion is slightly lower

[Real estate enterprise atlas] Zhongjun Group: land acquisition does not reduce financing cost by 6.4%

[Real estate enterprise atlas] Zhengrong Group: 7.4% financing cost, average profitability score

[Real estate enterprise atlas] Poly Real Estate slows down its land acquisition and long-term debt reaches 221.4 billion yuan

[Real estate enterprise atlas] High financing cost of contemporary real estate, average profitability

[Real estate enterprise atlas] The financing cost of Jiayuan International is up to 8.1%, and the pressure of debt repayment is highlighted

[Real estate enterprise atlas] High net debt ratio of COFCO Real Estate highlights short-term debt repayment pressure

[Real estate enterprise atlas] Greenland Holdings has greatly increased its land acquisition, with average profitability score

[Real estate enterprise atlas] Rongchuang's acquisition of land in half a year accounted for only 20% of the financing cost in 2017

Editor in charge: Li Yongfei