Topic: CITIC Securities Research: Investment Strategy in the Second Half of 2024

Stock speculation depends Jin Qilin analyst research report , authoritative, professional, timely and comprehensive, to help you tap potential theme opportunities!

Source: citic securities Research

writing | Qin Peijing, Qiu Xiang, Yang Fan, Ming Ming, Cui Rong, Yu Xiang

Distant Yang Jiaji, Li Shihao, Ma Xigaowa, Liu Chuntong

Zhou Chenghua, Wang Ximing Contact: Xu Guanghong

The three narratives of economic momentum conversion, capital market ecology, and Sino US strategic game that have suppressed the performance of A-share in the past three years will all usher in a major turning point. With the gradual verification of three kinds of signals, namely, policy, price, and external signals, the A-share market will usher in the starting point of an annual upward trend in the second half of 2024. The effectiveness of policies and the improvement of earnings quality are the main drivers, The investment paradigm of A-share in the next stage will be to desalinate the scale, attach importance to profitability, shift from the PEG framework of boom investment to the free cash flow growth premium, and improve the return on investment with high-quality development. It is suggested to grasp the strategic window to meet the big inflection point, and shift the allocation focus from low dividend to excellent growth step by step.

First of all, the three narratives that have suppressed the performance of A-shares in the past three years will all usher in a major turning point: First, the transformation of new and old economic drivers of "building before breaking" has begun to show results, and enterprises will weaken their scale, attach importance to profits, and avoid vicious competition under high-quality development; Second, the new "National Ninth Article" repositions the market investment and financing function, reshapes the market ecology based on investors, and improves the A-share return expectation; Third, the Libra of China US strategic game is leaning towards China, and China's strategic initiative is gradually strengthening, playing a more important role in global affairs.

Secondly, with the gradual verification of the three types of signals, the second half of the year will usher in the starting point of the annual upward trend of A-shares: in terms of policy signals, focus on the priority areas of the reform of the Third Plenary Session of the CPC Central Committee, and strengthen the new momentum of the economy with new quality productivity; In terms of price signals, under the smooth transition of old and new drivers, we will focus on observing the effect of stabilizing house prices and controlling production and ensuring prices in core cities; In terms of external signals, the global influence of the United States is gradually weakening, and China's diplomacy is taking the initiative to break the situation.

Finally, this round of market is expected to show three characteristics: logically, the market will shift from the expected repair drive to the reality verification drive; In terms of market catalysis, the third quarter will enter the signal observation period, where policy effect determines the rhythm, profit recovery determines the trend, and external factors determine the space; On the main line of the market, it is suggested to actively grasp the strategic window and gradually shift the focus of allocation from low dividend to high performance growth.

▍ Three inflection points: the three major narratives that have suppressed the performance of A-shares in the past three years will all usher in major inflection points.

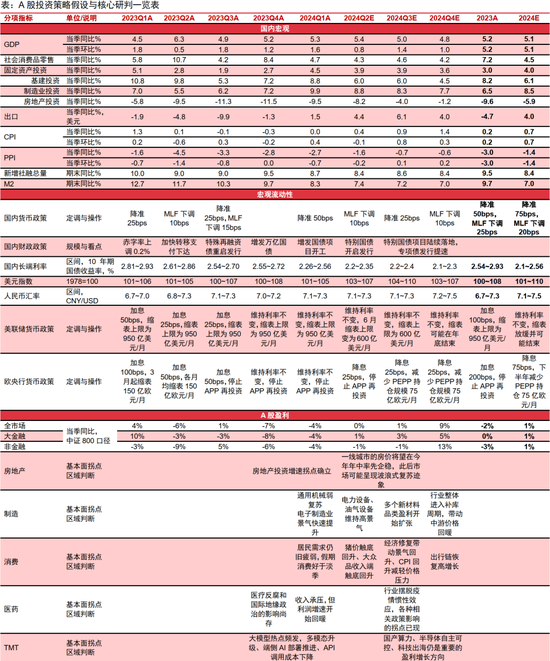

1) Turning point 1: The transformation of new and old economic drivers of "first establish before break" has begun to show results. Under high-quality development, enterprises will dilute scale, attach importance to profitability, and avoid vicious competition. On the one hand, judging by the significant changes in the relationship between real estate supply and demand, the real estate policy orientation has shifted from investment completion to demand increase and price stabilization. The real estate chain has walked out of the predicament under the support of policies, and the stage of the biggest drag on the economy has passed. According to the prediction of the real estate team of CITIC Securities Research Department, house prices in core cities are expected to stabilize in the middle of the year. After three years of continuous negative growth from 2022 to 2024, the growth rate of commercial housing sales area and real estate development investment is expected to rise back to near zero in 2025. On the other hand, as China's economy has entered a new stable state of high-quality development, the orientation of improving quality and reducing quantity has gradually become a consensus; In recent years, a large number of industrial policies have actively focused on scale control, encouraged market-oriented mergers and acquisitions, controlled production and guaranteed prices to avoid vicious competition. In the future, enterprises will weaken scale expansion and focus on improving profitability. The transformation of new and old drivers of China's economy has achieved initial results, and is expected to maintain a long period of medium high speed growth under the new stable state. With the above policies taking effect, the new quality productivity catalyzes the new drivers of the economy, A-share profitability and non-financial sector ROE will bottom out and recover, and ultimately improve the asset shortage pattern in the post real estate era in China.

2) Turning point 2: The new "National Ninth Rule" repositions the investment and financing function of the market, reshapes the market ecology based on investors, and improves the return expectation of A-shares. The new round of capital market "1+N" policy framework is becoming clearer with the implementation of the new "National Nine Rules". First of all, we should strictly control the "one in, one out" of the capital market, survival of the fittest in order to optimize the stock, and consolidate the basis for long-term returns of A-shares; According to Wind data, the total amount of A-share IPO and refinancing in the first five months of 2024 decreased by 83% and 70% respectively year on year, and the scale of major shareholders' reduction decreased by 79%. Secondly, strengthen supervision and punishment, pay attention to protecting investors and improve market stability; According to the summary of law enforcement issued by the CSRC, in 2023, the CSRC will investigate 717 cases of securities and futures violations, up 19% year on year, and impose 539 administrative penalties, up 40% year on year. Thirdly, the policy strongly guides dividend distribution. State owned enterprises pay more attention to market value assessment and directly improve investment returns. After the "New Company Law" came into effect on July 1 this year, capital reserves will be allowed to cover losses, which will facilitate the follow-up implementation of dividend distribution for excellent companies with negative undistributed profits. The policy of encouraging multiple dividend distribution may be conducive to the increase of dividend assets for insurance institutions. Finally, the reform should take multiple measures at the transaction end, financing end and investment end to reshape the market ecology, and the overall capital of the domestic primary and secondary markets ushered in an inflection point; According to our estimation, the supply and demand gap of A-share incremental funds in the third quarter of 2023 will be as high as 284.8 billion yuan (excluding retail investors and some institutional investors), while the net increase of funds in 2023Q4 and 2024Q1 will turn from negative to positive, which will be 310 billion yuan and 690 billion yuan respectively. The slowdown of equity financing, more standardized reduction of major shareholders' holdings, and the active entry of quasi "leveling" funds into the market are the main drivers of major inflection points of funds.

3) Turning point 3: The Libra of the Sino US strategic game is leaning towards China, and China's strategic initiative is gradually strengthening, playing a more important role in global affairs. First of all, under the anti globalization narrative, the "G2" of the strategic game between China and the United States, as a whole, is always strong, and is still the protagonist of the global economy; According to Wind data (the same below), the global share of GDP of both countries will increase from 39% in 2017 before trade friction to 42% in 2023. Secondly, in terms of trade, supported by industrial upgrading, supply chain advantages and export diversification strategy, China's export of goods in the world will increase from 12.8% in 2017 to 14.2% in 2023, and the proportion of manufacturing added value in the same period will increase from 26% to 31%. Under the A-share financial report, the overseas revenue of Chinese manufacturing enterprises has increased by more than 20% for three consecutive years in the past three years. Thirdly, in terms of science and technology, under the "small courtyard and high wall" type of precise sanctions of the United States, China has maintained its strategic determination and resilience and actively pursued. China's semiconductor capital expenditure has increased year by year in the global share, and projects such as the National Investment Fund for Integrated Circuit Industry have also provided strong financial support. Finally, in terms of finance, under the global security and multipolar demands, the slow de dollarization has weakened the influence of the United States, and the global central banks (except the Federal Reserve) will further increase the net purchase scale of reserve gold from 2022 to 2023; According to the International Monetary Fund (IMF), the proportion of US dollar assets in non gold reserve assets fell from 65% in 2016 to 58% in 2023; The proportion of RMB in international payments, trade financing and foreign exchange transactions has steadily increased in the past three years.

▍ Three types of signals: policy, price and external signals are gradually verified, and the second half of the year will usher in the starting point of annual level rising market.

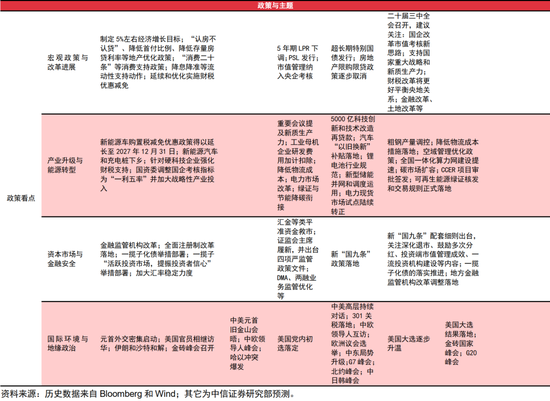

1) Policy signal: Focusing on the priority areas of the Third Plenary Session of the CPC Central Committee, new quality productivity strengthens the new driving force of the economy. First of all, it is expected that the Third Plenary Session of the CPC Central Committee in July will focus on further comprehensively deepening reform and promoting Chinese style modernization, and develop towards reform. Deepening reform and opening up is an important choice to deal with complex international and domestic situations and achieve high-quality development. Secondly, the following reform directions can be focused on: ① The new round of fiscal and tax system reform is expected to better balance the relationship between the central government and local governments and increase the proportion of direct taxes; ② Accelerate the construction of modern circulation system around logistics network, data elements and other aspects, and build a unified national market; ③ Adhere to the two "unswervingly" principles, which not only emphasize improving the core competitiveness and core functions of state-owned enterprises, but also improve the basic systems of market economy such as property rights protection, market access, fair competition and social credit. Finally, we should develop new quality productivity according to local conditions, strengthen the national scientific and technological strategic layout, build a modern industrial system through scientific and technological innovation, and promote the transformation and upgrading of the macro-economy.

2) Price signal. On the one hand, we should closely observe the effect of this round of real estate policies, especially the signals of marginal stability of house prices in core cities in the middle of the year. On May 17, the real estate policy was launched in a multi line manner, focusing on demand side support, focusing on purchase restriction and credit support. If the effect of this round of policy is not as expected, there is still room for the policy to be renewed in the year, and the policy of stock housing digestion is expected to continue to be strengthened. On the other hand, due to the deterioration of the competition pattern and price constraints, this year's economic recovery has been slow to transmit to corporate profits. Follow up, pay close attention to the effect of supply side production control and price protection policies, including: ① capacity control in traditional energy intensive industries; ② Emerging industries with rapid capacity growth before actively control capacity expansion; ③ Industries with a relatively stable competitive pattern have begun to focus on corporate profits and actively avoid vicious price competition.

3) External signal: the global influence of the United States is gradually weakening, and China's diplomacy is taking the initiative to break the situation. First of all, with the intensification of the policy swing of the United States and the decline of its global influence, its power vacuum and order imbalance appear in more regions of the world, resulting in frequent local geopolitical conflicts with strong sustainability. The Middle East, Russia, Ukraine and other geopolitical disturbances have increased significantly, and the situation in the Asia Pacific region is also surging. Secondly, no matter what the results of this year's presidential election in the United States are, due to the obvious split in the attitude of the American people on global issues, the credibility of the United States' commitment to global issues will systematically decline, the demands of third-party countries for strategic independence will increase, and the geopolitical influence of the United States and China will ebb and flow. Finally, it is expected that the political and economic value of the "Belt and Road" cooperation will continue to increase in the future. The EU will still attach importance to practical cooperation with China under the "strategic autonomy". The China Japan ROK Leaders' Summit may push the trilateral relations back on track gradually. In the second half of the year, China's diplomacy in all directions and fields is taking the initiative to break down, and is expected to play a more important role in global affairs.

▍ Three characteristics: policy effectiveness and improvement of earnings quality boosted A-shares, and the focus of allocation shifted from low dividend to high performance growth.

1) Market logic: The core drive of A-share has shifted from expected repair to reality verification. First of all, this round of active capital overweight entered the second half. According to the research on CITIC Securities channels, the position of the sample active private equity funds has risen rapidly from 67.8% to 77.8% since April, breaking the average level of 75% since 2017. There is limited space for further overweight in the future. Secondly, the equity valuation has been significantly repaired. The dynamic P/E of CSI 300 has recovered to 51% since 2010, and the dynamic P/E of Hang Seng Index has rebounded 20.2% from the bottom. Finally, the market driver has switched from expected improvement to reality verification. It is expected that under the guidance of high-quality development, enterprises will dilute scale expansion and attach importance to profitability, The improvement of ROE may become the most important feature of this round of profit cycle repair. We expect that after the bottom of the first quarterly report, the A-share earnings will show a slow recovery trend in 2024. It is expected that the year-on-year growth rate of the annual earnings (CSI 800 caliber) will rise from - 2% in 2023 to+1%. Manufacturing, science, technology and medicine with good domestic consumption and supply patterns are expected to become structural highlights of the year.

2) Market catalysis: policy effect determines the rhythm, profit recovery determines the trend, and external factors determine the space. With the disclosure of the A-share mid report and the clarification of the long-term reform expectations at the Third Plenary Session of the CPC Central Committee, we believe that there may be two scenarios for the market trend during the observation period of the three types of signals.

Scenario 1, The effect of the real estate policy exceeded expectations, and the reform plan of the Third Plenary Session of the CPC Central Committee was implemented quickly. In the third quarter, A-shares may directly start the annual level rise, with greater short-term flexibility. The main line of emerging industries that have priority to be catalyzed by the policy is expected to lead the rise. At the same time, overseas long-term allocated foreign capital will restart to flow in, domestic institutions and individual investors will usher in emotional resonance, public offering (including ETF) subscription and new issuance scale will recover, financing balance will rise, and the market will usher in significant incremental funds. Under this scenario, it is suggested to shift the focus of allocation to the theme of excellent growth and activity, and focus on those that are expected to receive priority policy catalysis Space space integration 、 Industrial intelligence and Biomanufacturing And so on.

Scenario 2:, The recovery effect of the real estate chain was not as expected, so it is necessary to wait for the real estate policy to exert again. With the implementation of the specific reform at the Third Plenary Session of the CPC Central Committee, the market will enter the consolidation period in the third quarter, and the A-share market in the fourth quarter may usher in the starting point of annual level rise. At the same time, it is expected that A-shares will maintain the game pattern of stock funds until the third quarter, and the flexible private placement position will gradually fall back to near the historical median, and the subjective bulls will continue to maintain a low dividend wave of certain positions as a defense; With the disclosure of the third quarter report clarifying the bottom of the A-share earnings cycle, the real estate policy continues to work. After the U.S. election in the fourth quarter, the external disturbance is expected to ease significantly. It is expected that flexible private placement will become active again, insurance funds will steadily enter the market, public offerings will gradually recover, and market liquidity will usher in a mild and continuous marginal improvement.

3) Main line of the market: It is suggested that the allocation focus in the second half of the year should gradually shift from low dividend to high performance growth. At present, the domestic macro rate of return is declining, and the economy has moved from a high growth stage to a high-quality development stage. Traditional boom investment, track investment, and industry trend investment are also facing a slowdown in growth and a reduction in catalytic events. Listed companies generally use capital expenditure and price war to achieve the goal of clearing up the industry, This also makes the subject satisfying investors' aesthetic under the PEG framework increasingly scarce. We believe that the investment paradigm of A-share in the next stage will be the stage of diluting scale, emphasizing profitability, shifting from the PEG framework of boom investment to free cash flow growth premium, and improving the return on investment with high-quality development. In terms of configuration, since three types of signals need to be observed in the second half of the year, it is still recommended to stick to the dividend strategy, focus on the stability of cash return, appropriately avoid industries with significant cyclical fluctuations in earnings and speculative capital intensity, and continue to focus on the stability of free cash return hydropower 、 nuclear power , the premium increases steadily Property insurance 。 With the continuous verification of the above three signals and the change of investment paradigm, the blue chip growth stocks represented by CSI 300 with the ability to continuously improve the growth of free cash flow may gradually dominate, focusing on banks (the expected improvement of asset quality opens up the space for revaluation) Mechanics (equipment renovation and sea going competition), home appliances (stable competition pattern, overseas business expansion and de real estate label) Electronics (Consumer Electronics Sailing, AI Innovation, Semiconductor Self control) new energy (Merger and reorganization, optimization of the pattern, and failure to go to sea) and other manufacturing leaders, with the industrial cycle bottoming out and stabilizing medicine (industrial integration, going to sea to break the situation) and Internet and consumer leader of Hong Kong stocks 。

▍ Risk factors:

The frictions between China and the United States in the fields of science and technology, trade and finance have intensified; Domestic policies or economic recovery is not as expected; Macro liquidity at home and abroad tightened more than expected; The conflict between Russia, Ukraine and the Middle East further escalated.

This article is excerpted from CITIC Securities Research Department on June 4, 2024 Published《 Investment strategy of A-share market in the second half of 2024 - meeting the big turning point 》See the report for detailed analysis contents (including relevant risk tips, etc.). In case of any ambiguity due to the excerpt of the report, the complete content of the report on the date of release shall prevail.

MACD Golden Cross signal is formed, and these stocks are rising well!

Massive information, accurate interpretation, all in Sina Finance APP

Editor in charge: Wei Yihan