Stock speculation depends Jin Qilin analyst research report , authoritative, professional, timely and comprehensive, to help you tap potential theme opportunities!

Strategy of Haitong Research

Key investment points

Core conclusions: ① This round of real estate optimization policy aims to digest the stock housing, optimize the incremental housing and prevent risks, which is more vigorous and more stable than in the past. ② The optimization of real estate policy is expected to boost sales and promote investment, and the real GDP growth rate is expected to reach about 5.5% under neutral circumstances. ③ The GDP repair and the weakening of the negative drag on the property chain will help to improve the earnings of A-shares. Under different circumstances, the net profit of all A-shares attributable to the parent company may be about 5-8% year on year.

Policy strength: a new round of comprehensive optimization. Recently, the State Council launched a series of heavy real estate optimization policies aimed at promoting the steady and healthy development of the market. These policies include lowering the threshold for house purchase, providing financing support, revitalizing the stock of housing, covering down payment ratio, loan interest rate, housing provident fund, de stocking and other aspects. Highlights include the lowest housing loan interest rate and down payment ratio in history, and the establishment of new policy financial instruments, such as 300 billion yuan of affordable housing refinancing. Compared with the loose policy in 2014-2016, this round of policy is more stable, more adaptable to the changes in the current market supply and demand relationship, and aims to meet housing demand while preventing risks.

Boost the economy: the real GDP growth is expected to be around 5.5%. A series of recent real estate optimization policies can boost the real estate market and support the economy. Measures such as lowering mortgage interest rate, down payment ratio and easing purchase restrictions will stimulate the release of residential demand for housing purchase; The government and state-owned enterprises help destocking. For example, the establishment of a loan support plan for rental housing will also increase the sales of new houses. Through regression analysis and prediction, it is estimated that under the assumption of optimistic, neutral and pessimistic policies, the sales area of commercial housing will reach 1.03 billion, 9.9 billion and 950 million square meters respectively this year, supporting the real GDP growth rate of 5.9%, 5.6% and 5.4% respectively.

Boost profitability: the growth rate of all A profits may reach 5-8%. Real estate and related industries have a significant impact on A-share earnings. Before 2016, the net profit attributable to the parent company of the real estate sector and the steel, construction and other industries driven by it accounted for about 10% of A-shares. In recent years, with the decline of real estate, the real estate and industrial chain have played a negative role in driving the earnings of A-shares, and the drag effect has been significant since 2021. In 2023, with policy support, the real estate fundamentals will improve, which is expected to help the earnings of A-shares recover. Under the assumptions of different real estate sales growth rates, it is expected that the year-on-year growth rate of A-share net profit attributable to the parent company will be 5% - 8%, and the contribution rate of the property chain to A-share earnings will be about - 1 to 1 percentage point.

Risk warning: The implementation of real estate policies was less than expected, and the domestic economic recovery was less than expected.

text

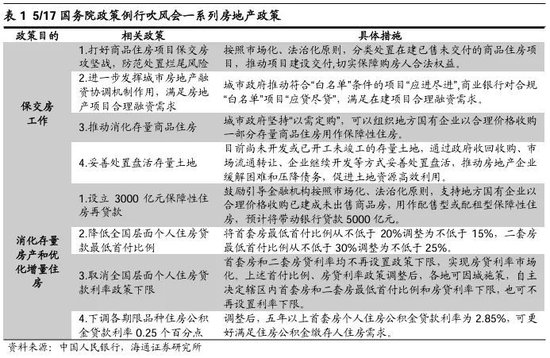

On May 17, several real estate policies were issued at the same time, and the market held extensive discussions on the policy content. If we want to implement the policy on the market, we need to discuss the effect of the policy from the fundamental aspects. In this report, we will analyze and calculate the role of this round of new real estate policies on economic growth and corporate profits in detail.

1. Policy strength: a new round of comprehensive optimization

Recently, the optimization and adjustment policies of real estate in many places have been implemented intensively. On May 17, the State Council Information Office held a regular briefing on the policies of the State Council, and a series of heavy real estate policies were introduced intensively, forming a combination of financial policies. The purpose is to promote the steady and healthy development of the real estate market through measures such as lowering the threshold for housing purchase, providing financing support, and revitalizing the stock of housing. The specific policy measures can be divided into two parts: ensuring the delivery of housing, digesting the stock of housing and optimizing the incremental housing.

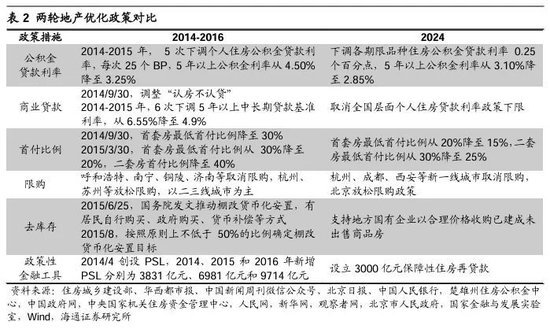

It can be seen that this round of policy adjustment covers the down payment ratio, loan interest rate, housing provident fund, inventory removal and other aspects, which shows the government's intention to comprehensively optimize the real estate market, with two highlights worthy of attention. On the one hand, both the housing loan interest rate and the down payment ratio fell to the lowest level in history, breaking the historical limit. From October 2014 to August 2015, China's provident fund loan interest rate fell from 4.5% to 3.25%, with a maximum decline of 25 BPs at a time, which is the same as the reduction this time. The minimum down payment ratio for the first set of housing is not less than 15%, and that for the second set of housing is not less than 25%. This is the lowest down payment ratio in history, and also the most relaxed policy among all kinds of housing purchase policies in recent years. On the other hand, new policy financial instruments should be set up to encourage the government to purchase and store existing houses. According to the idea of "government led and market-oriented operation", the People's Bank of China will provide 300 billion yuan of low-cost refinancing funds to encourage 21 national banking institutions to issue loans to local state-owned enterprises selected by the city government in accordance with the market-oriented principle, and the driving scale is expected to reach 500 billion yuan. Previously, the People's Bank of China has established a loan support plan for rental housing. The new tool is a continuation of the loan support plan for rental housing, which helps to promote the nationwide spread of the model of "market-oriented batch purchase of stock housing and expansion of rental housing supply".

So what is the strength of this round of real estate optimization policy compared with the previous one? The last round of China's real estate deregulation policy was intensively introduced in 2014-2016. We will compare the two rounds of real estate optimization policies.

In general, the two rounds of policies are aimed at boosting the real estate market by reducing the cost of housing purchase and increasing the investment of funds, but the specific measures and efforts are different, reflecting the changes in the market environment and regulatory objectives. In terms of credit easing, Both rounds of policies involve the reduction of down payment percentage, provident fund loan interest rate and commercial loan interest rate. The reduction was more frequent and larger in 2014-2016. Although this round of policies is relatively short, it has broken through the lower limit of down payment percentage and provident fund loan interest rate. At the same time, the lower limit of commercial loan interest rate has been canceled, giving the market greater autonomy. In terms of easing purchase restrictions, The two rounds of policies have shown the trend of easing purchase restrictions, but there are some differences in the scope of cities and the specific contents of the policies. From 2014 to 2016, the easing of fixed year purchase restrictions is mainly concentrated in second and third tier cities, while this round of policies has seen the easing of purchase restrictions in first tier and new first tier cities. In terms of de stocking, Both rounds of policies have taken measures to promote the de stocking of the real estate market, but the methods may be different. From 2014 to 2016, the de stocking was mainly through monetization of shed reform, while this round encouraged local state-owned enterprises to purchase to digest the inventory. In terms of policy financial instruments, After the establishment of PSL in 2014, the cumulative distribution of PSL from 2014 to 2016 exceeded 2 trillion yuan, which was of a large scale, accounting for 65% of the whole source of funds for shantytown reconstruction; This round of the central bank set up affordable housing refinancing, with an initial investment of 300 billion yuan and a moderate scale. It is expected to leverage bank loans of 500 billion yuan, adding to the 500 billion yuan PSL used for "three major projects" at the end of last year, the market funds are reasonable and abundant.

In general, this round of real estate optimization policy is more stable, more suitable for the current background of "significant changes in the supply and demand relationship of the real estate market", re-examine and adjust the restrictive policies introduced in the long-term overheating stage of the market, and prevent risks and speculation while meeting the rigid and improving housing needs of residents.

2. Boost the economy: real GDP growth is expected to be around 5.5%

Before the launch of this round of real estate policies, as of the end of the first quarter, the real estate industry had dragged down GDP by about 0.38 percentage points. Since 2021, China's real estate sales, production and investment have all fallen from the high point, which has lasted for nearly three years. The downturn of real estate also has a significant drag on the economy. Since the real estate policy was tightened in 2021, the real estate industry has dragged down the GDP by 0.27% and 0.08% respectively in 2022 and 2023. Since this year, with the further decline of real estate investment and sales, the drag of real estate on the economy has also intensified. By the end of April, before the introduction of intensive policies, the cumulative year-on-year growth rates of China's commercial housing sales area, housing newly started area, and real estate development investment completed amount were - 20.2%, - 24.6%, and - 9.8%, respectively, with a further increase in the decline compared with the end of last year, which also aggravated its drag on the economy. From the data of the first quarter, the single real estate industry dragged down the GDP by 0.38 percentage points. In the period of transformation of new and old driving forces, in addition to pursuing the "advancement" of new quality productivity, it is also necessary to take into account the "stability" of traditional industries such as real estate, which is also an opportunity for a series of recent real estate optimization policies.

What will happen to the fundamentals and economic data of real estate after the introduction of the real estate optimization policy? We measured different policy situations. Our analysis idea is to conduct regression analysis based on historical data, calculate the pull parameters of various optimization policies on real estate and economic data, and predict the effects of policy combinations with different strengths. Logically speaking, the commencement and investment of real estate are lagging behind the sales of new houses. The most direct effect of the real estate optimization policy is to boost sales, thus stimulating subsequent commencement and investment. However, from the actual data, the leadership of sales is not obvious, and the sales, commencement and investment indicators show a trend of synchronous change, with a high correlation between the three. Since the analysis of the impact of policies on sales is the most intuitive among the three indicators, we need to first measure how the real estate sales will change under different policy assumptions.

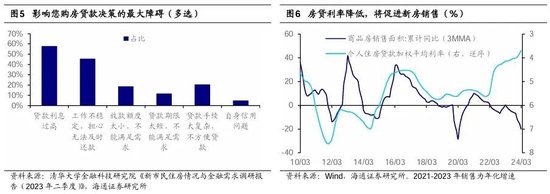

On the one hand, there is still some housing demand on the residential side that can be released. In the special report of Haitong's total volume, "Thinking about the transformation of China's new and old drivers: learning from the 98-00 years", we once made a simple calculation that China's new citizens, such as college graduates and migrant workers, are large in size, with a stock of nearly 300 million people, and the size is increasing every year (more than 7.5 million people), which still has a certain potential demand for housing. According to the questionnaire results in the Research Report on Housing Conditions and Financial Needs of New Citizens (the second quarter of 2023), we found that the main factors restricting new citizens to borrow and buy houses are the high housing loan interest rate and the low loan limit. Then, measures such as lowering the mortgage interest rate and down payment ratio, and easing purchase restrictions can lower the threshold for house purchase, increase the number of potential buyers, and help stimulate the release of rigid demand and improved housing demand.

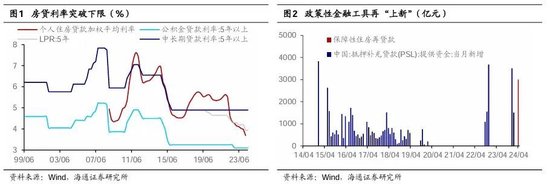

Lowering the interest rate of house purchase loans can reduce the pressure on residents to repay debts in each period and increase housing sales. At present, the weighted average interest rate of Chinese residents' personal housing loans is 3.69%, and the interest rate of provident fund loans for more than five years is 3.1%. If the interest rate is reduced by 0.25 percentage points, the monthly repayment amount of 1 million loans will be reduced by about 500 yuan, which can improve residents' willingness to buy houses to a certain extent. According to historical data, we find that there is a high negative correlation between the sales area of commercial housing and the weighted average interest rate of individual housing loans. After linear regression, we found that the weighted average interest rate of residential housing loans decreased by 1 percentage point, which could increase the area of housing purchase by 48.35 million square meters. Referring to the extent of the decline of the housing loan interest rate in the initial period of the policy adjustment in 2014 (0.7 percentage points in the fourth quarter of 2014), and combining the current reality, We have assumed an optimistic, neutral and pessimistic situation, that is, by the end of this year, the weighted average interest rate of residential housing loans will gradually decline to 3.3%, 3.4% and 3.5%, so the sales area of commercial housing will increase by 37.47 million, 27.87 million and 18.26 million square meters this year.

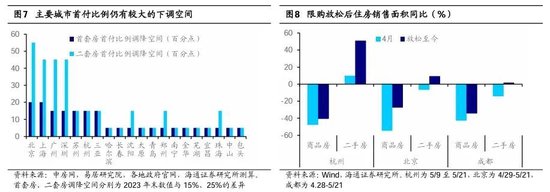

Reducing the down payment percentage can reduce the current expenditure of residents on housing purchase and lower the threshold for housing purchase access. According to the data of Yiju Research Institute in 2023 quoted by Nanjing Housing Security and Real Estate Bureau, Beijing News and Xinhua News Agency, the average down payment ratio of first set of housing in 20 key cities across the country is 24%, and the average down payment ratio of second set of housing is 42%. There is still some room for the lower limit of 15% and 25% policies. In the past year, the proportion of down payment for house purchase in various regions has been gradually reduced. According to the data of Shell Research Institute quoted by Securities Times, in the fourth quarter of 2023, the average proportion of commercial loans in key cities will be 64.1%, 2.4 percentage points higher than that in the same period of 2022, and 1.5 percentage points higher than that in the third quarter of the same year. Increasing the loan ratio can enable residents to leverage more under the same funds, thus increasing the number of house purchases. We assume that under optimistic, neutral and pessimistic conditions, the actual down payment proportion of residents decreases by 1%, 1.5% and 2% respectively, and accordingly, the funds that can be leveraged by the same down payment funds increase by 2.9%, 4.4% and 5.9% respectively. With the unit price unchanged, it means that the residential area will increase by the same proportion.

Relaxation of purchase restriction policy has relatively limited effect on new house sales. Here we list three cities that have optimized the purchase restriction policy recently, Chengdu (April 29), Beijing (April 30) and Hangzhou (May 9). Relatively speaking, the optimization of the purchase restriction policy is more significant for the sales of second-hand houses at present, and the improvement of the sales of first-hand houses is relatively small. Even in Hangzhou, where the purchase restriction has been relaxed for a short time, the sales of new houses do not increase but decrease year-on-year. Whether the purchase restriction policy can stimulate demand depends on the cooperation of other policies.

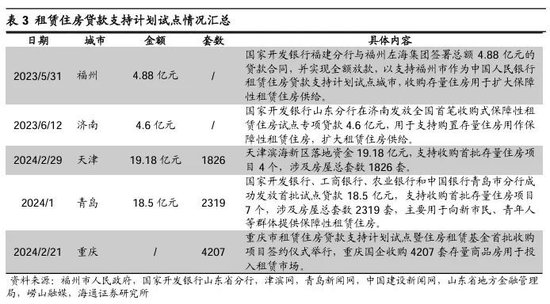

Secondly, the assistance of the government and state-owned enterprises in destocking can also lead to some new sales, including local state-owned enterprises' purchase of stock commercial housing, revitalization of stock land, etc., supported by financial institutions. In February 2023, the People's Bank of China printed and distributed the Notice on Launching the Pilot Loan Support Plan for Rental Housing, established the "Rental Housing Loan Support Plan", with the amount of 100 billion yuan, and granted loans for rental housing purchase to eight pilot cities in Chongqing, Jinan, Zhengzhou, Changchun, Chengdu, Fuzhou, Qingdao, and Tianjin. As of March this year, five cities have invested 4.716 billion yuan to purchase 8352 commercial housing stocks, with an average price of 910000 yuan/set. Under optimistic, neutral and pessimistic circumstances, we respectively assume that the scale of fully released affordable housing refinancing in the year will be RMB 4000, 300 and 200 billion, and according to the proportion of the central bank "granting refinancing at 60% of the loan principal", we can respectively leverage bank loans of RMB 666.7, 500 and 333.3 billion, calculated based on the average area of each house of 100 square meters, It can increase the newly increased housing area by 7334, 5500 and 36.67 million square meters respectively.

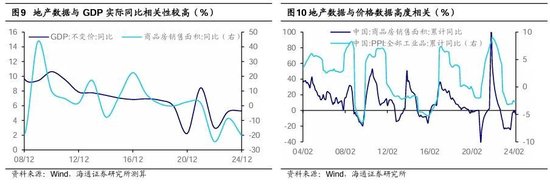

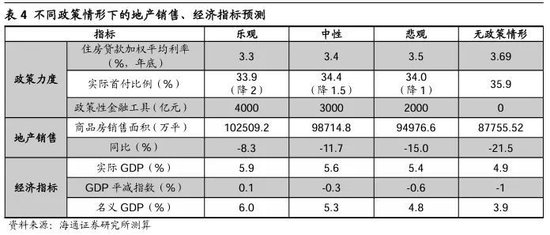

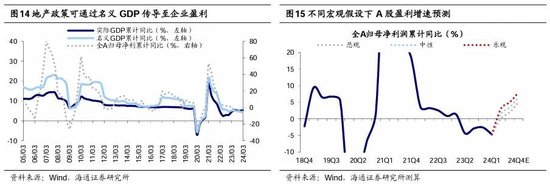

According to the predicted value of the real estate data under different policy situations, we can further predict the economic data. On the one hand, there is a high correlation between real estate sales and real GDP. From the perspective of the production method, except that the added value of the construction industry and the real estate industry is directly linked to the basic data of the real estate, other real estate related industries will also be affected. On the other hand, changes in real estate will also affect prices. From the historical data, it can be seen that there is a high correlation between the real estate sales area and PPI, which is mainly due to the growth of real estate supply and demand, which will increase the demand for energy, building materials, machinery and other industrial products, thus raising the price. The PPI is also highly correlated with the GDP deflator, so we can predict the GDP deflator based on the real estate data in different situations. Through simple linear regression, we forecast the economic data under the three policy scenarios. The specific results are shown in Table 4. Under the neutral policy assumption (the housing loan interest rate drops to 3.4%, the actual down payment proportion drops by 1.5 percentage points, and the 300 billion yuan affordable housing refinancing is implemented), the actual GDP growth rate may reach 5.6%, and the GDP deflator is - 0.3%, making the nominal GDP growth rate reach 5.3%.

3. Boost profitability: the growth rate of all A profits may reach 5-8%

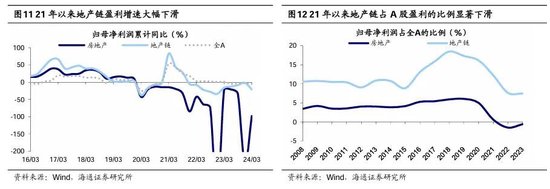

Real estate and related industries have an important impact on A-share earnings. Real estate is an important pillar of the macro-economy and an important part of listed companies. Before 2016, the proportion of the real estate sector's net profit attributable to the parent company in all A-shares was basically maintained at around 4%. If the driving effect of real estate is taken into account and the related industries such as steel, construction, building materials, household appliances, household appliances, etc. are included in the calculation, the proportion of the real estate chain's net profit attributable to the parent company in all A-shares is basically maintained at around 10%. After 2016, supported by factors such as shantytown reform, the profits of the real estate chain increased rapidly, and the proportion of the real estate chain in A-share profits also rose to a new height. On the whole, the profit share of the real estate in 2016-2020 was basically maintained at around 5.5% and once reached 6.1%, while the profit share of the real estate chain was basically maintained at around 16.2% and once reached 18.5%.

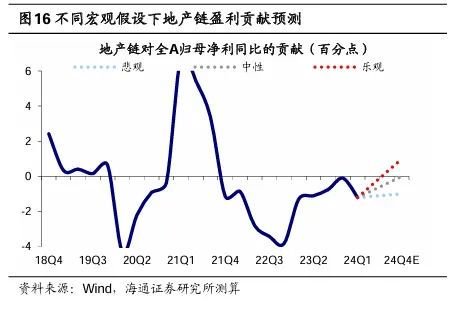

In recent years, the property chain has played a significant negative role in pulling A-share earnings. After 2021, as the real estate entered a downward cycle, the fundamentals of the real estate chain weakened. The year-on-year growth of the net profit attributable to the parent of the real estate sector continued to be negative, and even began to suffer losses. The proportion of profits also fell from 5.0% in 2020 to - 0.6% in 2023, while the net profit attributable to the parent of the real estate chain fell from a high point of 83.1% in 21Q1 to - 34.3% in 22Q4, Since then, although it has recovered, it is still in negative growth, and the proportion of profits has also declined from 16.2% in 2020 to 7.5% in 2023. We further analyze the driving effect of real estate and related industries on A-shares. We need to combine the proportion of the real estate chain in A-shares and its growth rate. Through measurement, we can find that since 2021, the real estate and the real estate chain have significantly slowed down the earnings growth of A-shares. In 2021, they will drag down 3.0 and 1.1 percentage points of the total A-share net profit respectively, and in 2022, they will drag down 1.5 and 3.8 percentage points respectively, In 2023, they will drag down 0.4 and 0.1 percentage points respectively. It should be noted that in 2023, the negative pull of the real estate chain will ease, mainly due to the recovery of profits in the construction industry, or related to the power of infrastructure under the stable growth policy. After excluding construction, the real estate chain will drag 0.5 percentage points.

With policy support, the improvement of real estate fundamentals may help the recovery of A-share earnings. According to the above analysis, the property chain has a great drag on A-share earnings. If the fundamentals of the property chain improve, to what extent can it help A-share earnings recover? With policy support, the improvement of the fundamentals of the real estate chain is conducive to the recovery of the domestic economy, and nominal GDP is expected to achieve faster growth, while A-share earnings are closely related to nominal GDP growth. According to Haitong's macro analysis above, under the three assumptions of pessimistic, neutral and optimistic growth of real estate sales area, the nominal GDP is expected to achieve a year-on-year growth of 4.8%, 5.3% and 6.0% respectively, and we expect that all A-share net profits attributable to the parent company will achieve a year-on-year growth of about 5%, 6.7% and 8% respectively. Further, we analyze the driving effect of the property chain on A-share earnings. Historically, at the stage of rapid recovery and high growth of real estate sales (such as 2009, 2013 and 2016), the contribution rate of the real estate chain to A-share earnings can increase by about 3-5 percentage points, while at the stage of slow stabilization of real estate sales (such as 12 and 15 years), the contribution rate of the real estate chain to A-share earnings can increase by about 1-2 percentage points. The contribution rate of the 24Q1 property chain to the accumulated net profits of all A-shares attributable to the parent company on a year-on-year basis is - 1.2 percentage points. In combination with the historical situation and the current real estate situation, it is estimated that under the three assumptions of pessimism, neutrality and optimism, the contribution rate of the property chain to the earnings of A-shares is about - 1, 0 and 1 percentage points respectively.

Risk warning: The implementation of real estate policies was less than expected, and the domestic economic recovery was less than expected.

This article is selected from Haitong Securities Research report of the Research Institute: Haitong Total | Measurement of the impact of the new real estate policies on the economy and profitability

Published on: May 23, 2024

When the stock market recovers, open an account first! Intelligent fixed investment, condition sheet, individual stock radar... for you>>

Sina statement: This message is reproduced from Sina's cooperative media. The purpose of posting this article on Sina.com is to convey more information, and does not mean to agree with its views or confirm its description. The content of this article is for reference only and does not constitute investment advice. Investors operate accordingly at their own risk.

Massive information, accurate interpretation, all in Sina Finance APP

Editor in charge: Ling Chen