On collapse

The yen fell to a new record low today, which is the situation after the Bank of Japan meeting. We believe that this situation is reasonable, which also indicates that the market has finally realized that Japan is implementing a kind of friendly policy of ignoring the yen.

For a long time, we have believed that foreign exchange intervention has no credibility. From the perspective of credibility, the statement of the Minister of Finance last night was generally positive

If the market becomes chaotic, the possibility of foreign exchange intervention cannot be completely ruled out, but it is worth noting that the governor of the Bank of Japan played down the importance of the yen at today's press conference and said that there is no urgency to raise interest rates.

In this context, we will describe the current collapse of the yen from the following points:

1. For Japan, the weak yen is not so bad.

The tourism industry is booming, the Nikkei index profit rate is rising, and the competitiveness of exporters is enhanced. Indeed, the cost of imported goods has risen. However, the growth is good, the government is helping offset some costs through subsidies, and core inflation has not accelerated. More importantly, Japan has a large number of foreign assets with its positive international investment position.

Therefore, the weakening of the yen has brought huge capital gains to foreign bonds and stocks. The most intuitive example is that the profits of the Government Pension Fund (GPIF) in the past two years have exceeded the total of the previous two decades.

2. Japan has no inflation problem.

Japan's core CPI is about 2%, which has been declining in recent months. Excluding the one-time impact, the Tokyo consumer price index released last night was 1.7%.

Indeed, inflation may accelerate again due to weaker exchange rates and wage growth. However, compared with the post epidemic interest rate increase cycle of the Federal Reserve and the European Central Bank, the starting point of inflation is completely different.

Therefore, inflation brings less pressure and the urgency of raising interest rates is low. The most obvious evidence is that Japanese consumer confidence is close to a cyclical high.

3. Negative real interest rate is very favorable.

Maintaining negative real interest rates is very attractive for integrating the government balance sheet. As we proved last year, this created fiscal space through the $2000 trillion arbitrage trade, and created asset returns for Japan's wealthy voters.

This has promoted the domestic capital outflow that we have been emphasizing in the past year, which is a key factor for the weakening of the yen and also makes Japan's broad basic income and expenditure one of the weakest in the world. It is not speculators who weaken the yen, but the Japanese themselves.

The decline of the yen has become disorderly, which indicates that there may be a final, possibly sharp decline before reaching the bottom.

As widely expected, the Bank of Japan did not change interest rates at today's policy meeting, although they did raise their inflation forecast. The forecast for fiscal year 2025/26 shows that the core inflation rate (excluding food and energy) is 2.1%, and the real GDP growth is 1%.

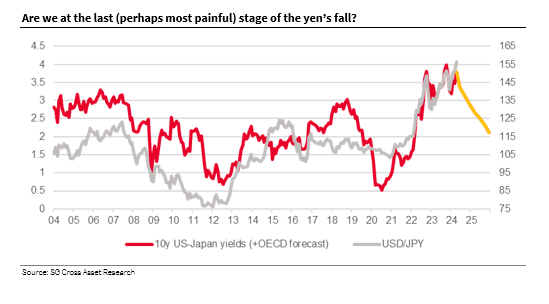

Japan, like most countries, tends to have higher bond yields than nominal GDP growth in the long run. On this basis, the income gap between USD and JPY will be significantly narrowed in the coming quarters.

However, At present, US yields are rising, while Japanese yields are still supported by very low short-term interest rates. These low short-term interest rates have provided positive returns for short yen trading, making the leveraged trading community optimistic in the past few months.

The chart shows the relationship between the US dollar/yen exchange rate and the US Japan income gap over the past 20 years. The income chart is extended by using the OECD's forecast of income.

These are just forecasts, but they frame the problem quite well, especially considering the extent to which the yen is currently undervalued, regardless of any basic long-term valuation.

If the purchasing power parity of USD/JPY is now at the mid 90 level, even after the exception theory and Japanese adjustment in the United States, the fair value is still about 110. As long as the income gap is large and continues to expand, the dollar/yen will still face upward pressure and eventually return to around 110.

The risk here is that unless Japanese policy makers take more active action (intervention and monetary policy), the rising momentum of USD/JPY may end in an excessive surge.

VIP course recommendation

APP exclusive live broadcast

Popular recommendation