Editor's Note: On October 30, the IPO of Suzhou Longjie Special Fiber Co., Ltd. (hereinafter referred to as "Suzhou Longjie") was approved. Suzhou Longjie plans to issue no more than 29.735 million shares in the Shanghai Stock Exchange. The sponsor is Guosen Securities 。 Suzhou Longjie plans to raise 500 million yuan for green composite fiber new material production project, high-performance special fiber R&D center project, and replenish working capital. This is the second IPO of Suzhou Longjie. It is reported that Suzhou Longjie applied for IPO in 2012 and withdrew the application in March 2013.

From 2014 to January June 2018, the operating revenue of Suzhou Longjie was 1.331 billion yuan, 1.443 billion yuan, 1.207 billion yuan, 1.524 billion yuan and 808 million yuan respectively, and the net profits attributable to the shareholders of the parent company were 55.6568 million yuan, 176 million yuan, 63.9776 million yuan, 135 million yuan and 75.8328 million yuan respectively.

Suzhou Longjie expects its operating revenue from January to September 2018 to be 1.218 billion yuan - 1.339 billion yuan, up 9.52% - 20.36% year on year; Net profit was 116 million to 128 million yuan, up 16.14% - 27.34% year on year.

This time, the raised capital of 50 million yuan will be used for the "supplementary working capital" of Suzhou Longjie raised investment project. However, during the reporting period, Suzhou Longjie paid dividends for many times, with a total of 202 million yuan.

From 2014 to June 30, 2018, the monetary capital of Suzhou Longjie was 58.2229 million yuan, 92.3396 million yuan, 61.6374 million yuan, 158 million yuan and 72.9343 million yuan, respectively, accounting for 18.52%, 23.44%, 17.43%, 30.30% and 12.32% of current assets.

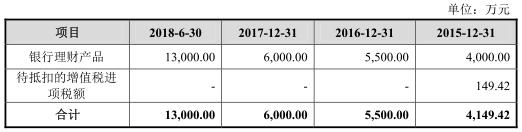

From 2015 to June 30, 2018, the amount of financial products of Suzhou Longjie Bank was 40 million yuan, 55 million yuan, 60 million yuan and 130 million yuan respectively.

From 2015 to June 30, 2018, the total amount of notes receivable and accounts receivable of Suzhou Longjie was 54.32 million yuan, 60.0983 million yuan, 145 million yuan and 226 million yuan respectively.

During the reporting period, the balances of accounts receivable of Suzhou Longjie were 15.5885 million yuan, 16.5317 million yuan, 12.8292 million yuan, 6.6313 million yuan and 6.3246 million yuan, respectively. The accounts receivable accounts for 1.17%, 1.15%, 1.06%, 0.44% and 0.78% of the current operating revenue. The turnover rate of accounts receivable was 78.58 times, 89.82 times, 82.23 times, 156.59 times and 124.76 times respectively. The notes receivable of Suzhou Longjie are bank acceptance bills, with the amount of 38.6946 million yuan, 48.1723 million yuan, 139 million yuan and 221 million yuan respectively.

From 2014 to June 2018, the inventory of Suzhou Longjie was 110 million yuan, 174 million yuan, 155 million yuan, 143 million yuan and 146 million yuan respectively, accounting for 35.10%, 44.14%, 43.71%, 27.49% and 24.59% of current assets, respectively. The inventory turnover rate was 10.32 times/year, 8.07 times/year, 6.36 times/year, 8.43 times/year and 4.58 times/year, respectively. Suzhou Longjie has a large amount of goods in stock, which are 76.7925 million yuan, 122 million yuan, 124 million yuan, 106 million yuan and 95.7194 million yuan respectively.

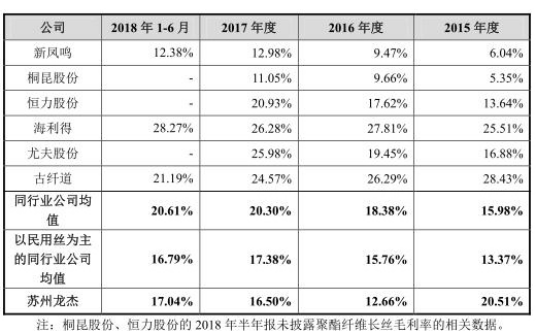

From 2014 to January June 2018, the comprehensive gross profit margin of Suzhou Longjie was 10.90%, 20.49%, 12.92%, 16.56% and 17.08% respectively, and the gross profit margin of its main business was 10.95%, 20.51%, 12.66%, 16.50% and 17.04% respectively.

From 2015 to January June 2018, the average gross profit margin of polyester filament products of comparable companies in the same industry was 15.98%, 18.38%, 20.30% and 20.61%. The gross profit rate of Suzhou Longjie's main business in 2015 was higher than the average of the industry, and the gross profit rate of its main business in 2016, 2017 and January June 2018 was lower than the average of the industry.

In 2016, the sales price of Suzhou Longjie suede fiber series products dropped by 23.70%. From 2015 to January June 2018, the sales prices of suede fiber series products were 13800 yuan/ton, 10500 yuan/ton, 12600 yuan/ton and 13300 yuan/ton respectively.

From 2014 to June 2018, the total liabilities of Suzhou Longjie were 304 million yuan, 232 million yuan, 191 million yuan, 201 million yuan and 175 million yuan respectively. The asset liability ratio of Suzhou Longjie was 41.00%, 29.24%, 26.61%, 24.07% and 19.79%, respectively. The asset liability ratio declined and was lower than the average of the industry, so it had strong solvency. From 2015 to June 30, 2018, the average asset liability ratio of companies in the industry was 51.45%, 47.16%, 46.67% and 43.49%, respectively.

Suzhou Longjie has secured 8 houses and buildings with property right certificates, and has 3 land use rights, all of which have been mortgaged.

During the reporting period, Wang Jianfang, a related party of Suzhou Longjie, and Zhangjiagang Shengji Freight Co., Ltd. under its control provided goods transportation services to Suzhou Longjie. The transaction amounts were 1310900 yuan, 709900 yuan, 1825700 yuan, 1061400 yuan and 341000 yuan, respectively, accounting for 19.06%, 10.95%, 30.04%, 19.20% and 12.94% of the current transportation costs.

Suzhou Longjie also had the situation of entrusted payment of loan funds through related parties. After the bank released the loan funds to the company's account, the company transferred the loan funds to the Longjie investment account under the supervision of the bank, and Longjie Investment re transferred the loan funds back to the company's account within a short time after receiving the funds.

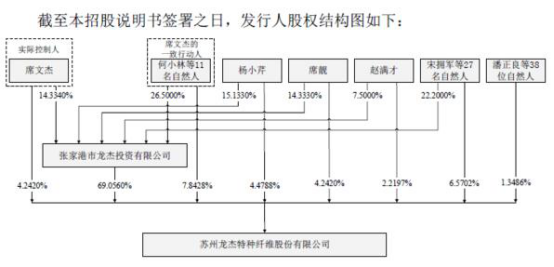

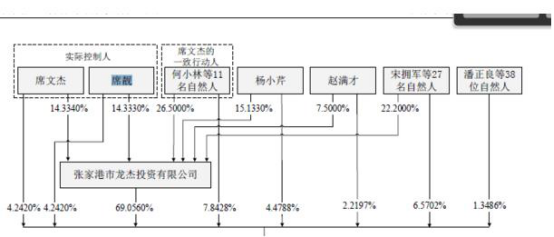

The control of Suzhou Longjie is also quite a story. Among the shareholders of Longjie Investment, Yang Xiaoqin, a natural person shareholder with the highest shareholding ratio, is 15.13%, while she also has a direct shareholding ratio of 4.48% in Suzhou Longjie Investment. The total direct and indirect shareholding ratio can reach 14.93%, which is the natural person shareholder with the highest shareholding ratio. However, the actual controller of Suzhou Longjie disclosed at that time was Xi Wenjie, Yang Xiaoqin's ex husband.

In the latest prospectus, the actual controller of Suzhou Longjie became "Xi Wenjie and his daughter Xi Liang". In addition, Xi Wenjie also signed the Agreement of Concerted Action with 11 shareholders. Finally, Xi Wenjie and Xi Liang jointly controlled 85.38% of the voting rights of Suzhou Longjie. And will having such a high number of ex-wife shareholders in the company have an impact on control?

According to Phoenix. com, Ningbo Hongwan Home Textile Products Co., Ltd. is the largest customer of Suzhou Longjie, and also the second largest bill receivable customer. Ningbo Hongwan actually includes three companies, namely Ningbo Hongwan Home Textile Products Co., Ltd., Ningbo Beiwei Textile Co., Ltd., and Ningbo Weiyi Long Wool Co., Ltd.

According to Tianyan's data, Ningbo Beiwei Textile Co., Ltd. was publicized as a dishonest company by the Supreme People's Court, and was sentenced to pay 7.1941 million yuan of execution fee and interest, bear 63370.55 yuan of execution fee, pay 8 million yuan of loan and interest, and advance principal of 2.7728 million yuan and interest. In addition, according to the information query of the people subjected to enforcement by the national courts, the Cixi People's Court enforced the assets of Ningbo Beiwei Textile Co., Ltd. of 68 million yuan.

Yu Wanjun, the chairman of Beiwei Changmao Company, also served as the chairman of Beiwei Textile, and Beiwei Textile Company is the old Lai announced by the Supreme Law. Yu Wanjun and Long Jie Chairman Xi Wenjie are members of the China Wool Textile Industry Association, and have successively served as the executive deputy directors of the second and third artificial fur professional committees.

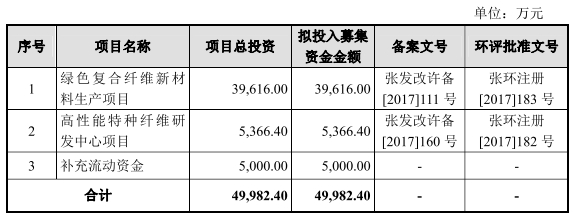

The introduction of Suzhou Longjie raised investment project shows that of the nearly 500 million yuan raised this time, 397 million yuan will be used for the "green composite fiber new material production project", which will increase the production capacity of 50000 tons/year polyester fiber filament, mainly PTT fiber and composite fiber.

From the time and technical reserves of Suzhou Longjie entering the PTT fiber field, Suzhou Longjie does not have obvious advantages. The prospectus shows that the company has 63 patents and 4 trademarks, but most of these patents are related to the previous key product series, and only 3 patents are related to the PTT fiber series.

The average selling price of fiber products of Suzhou Longjie is far higher than that of other listed companies in the same industry. The explanation given in this prospectus is that "products produced by different production processes are different", that is, the chip spinning process adopted by Suzhou Longjie can produce products with high technology content, multiple functional requirements and complex structure.

However, the chip spinning process of Suzhou Longjie is regarded by peers as being eliminated. One of the representative companies in the same industry announced by Suzhou Longjie is New Fengming In its prospectus, Xin Fengming disclosed that in recent years, "the operating rate of enterprises adopting the chip spinning process has differentiated from that of enterprises adopting the melt direct spinning process", and "the chip spinning process has higher energy consumption, less production stability than the melt direct spinning process, and the melt direct spinning process has gradually replaced the chip spinning process".

In addition, according to the prospectus of Xinfengming, "Xinfengming Chemical Fiber was originally a subsidiary of Xinfengming that produced polyester filament by chip spinning, and its business premises were located in the above implementation scope. In response to the government's development strategy of improving the urban environment, optimizing the industrial structure, and accelerating economic transformation and upgrading, Xinfengming Chemical Fiber stopped the original polyester filament business". Under the environment of increasingly strict environmental protection inspection and limited energy consumption industry, will Suzhou Longjie, which uses the chip spinning process, face the risk of forced elimination in the future?

The reporter of China Economic Network sent an interview letter to Suzhou Longjie Securities Department, but no reply has been received as of press release.

Apparel and home textile fabric provider is proposed to be listed in Shanghai Stock Exchange

Suzhou Longjie Special Fiber Co., Ltd. (hereinafter referred to as "Suzhou Longjie") has been focusing on the research, development, production and sales of differentiated and new polyester filaments such as differentiated polyester filaments and PTT fibers. The company's products have gradually developed from early differentiated varieties such as silk imitation and cotton imitation to differentiated and new polyester fiber products focusing on suede like fiber, fur like fiber, PTT fiber, etc., which are mainly used in the production of clothing and home textile fabrics such as imitation animal fur, suede like fabric, memory fabric, etc.

From 2014 to January June 2018, the operating revenue of Suzhou Longjie was 1.331 billion yuan, 1.443 billion yuan, 1.207 billion yuan, 1.524 billion yuan and 808 million yuan respectively, and the net profits attributable to the shareholders of the parent company were 55.6568 million yuan, 176 million yuan, 63.9776 million yuan, 135 million yuan and 75.8328 million yuan respectively.

Suzhou Longjie expects its operating revenue from January to September 2018 to be 1.218 billion yuan - 1.339 billion yuan, up 9.52% - 20.36% year on year; Net profit was 116 million to 128 million yuan, up 16.14% - 27.34% year on year; The net profit attributable to common shareholders of the Company after deducting non recurring profit and loss was 106 million yuan to 117 million yuan, up 15.83% - 28.16% year on year.

In 2016, the number of Suzhou Longjie employees decreased significantly. During the reporting period, the number of registered employees of Suzhou Longjie was 1148, 1598, 1214, 1283 and 1309 respectively. Suzhou Longjie said that it was mainly because the company stopped leasing Changjiang Plastics in 2016, and the branch stopped production. The number of employees of the company changed in line with the business development trend.

The controlling shareholder of Suzhou Longjie is Longjie Investment, which holds 69.06% of the company's shares. The actual controller is Xi Wenjie and his daughter Xi Liang. Xi Wenjie is the chairman and general manager of the current company. He directly holds 4.24% of the company's shares and 14.33% of the company's controlling shareholder Longjie Investment, and controls 7.84% of the company's shares and 26.50% of Longjie Investment's shares through concerted action arrangements. Xi Liang is an employee of the securities department of the current company. He directly holds 4.24% of the company's shares and 14.33% of the company's controlling shareholder Longjie Investment. As of August 24 this year, when the prospectus was signed, Xi Wenjie and Xi Liang controlled 85.38% of the company's shares through shareholding and concerted action arrangements.

Xi Wenjie, born in 1966, Chinese, without permanent residency abroad, holds a master's degree. From 1988 to 1998, he successively served as the technician, workshop director, head of Biotechnology Section, assistant to the general manager, and deputy general manager of Zhonggang Group; From 1999 to 2003, served as the director of Zhonggang Specialty Chemicals Factory; From June 2003 to May 2011, he served as the executive director and general manager of Longjie Co., Ltd; From January 2011 to now, he has been the executive director of Longjie Investment; Since May 2011, he has served as the chairman and general manager of the company.

Xi Liang, born in 1989, Chinese, without permanent residency abroad, is now an employee of the company's securities department.

It is worth noting that in the prospectus submitted by Suzhou Longjie Daily on September 15, 2017, Xi Liang was not identified as the actual controller of the company. In response, the IEC required Suzhou Longjie to disclose in its feedback: (1) the reason and rationality of identifying Xi Wenjie as the actual controller only; (2) Whether the actual controller of the issuer has equity disputes with the original spouse, and whether the original spouse and her daughter have concerted action arrangements; (3) Whether the actual controller of the issuer has changed, if not, please explain the basis; (4) Please describe Xi Wenjie's actual control over the company in combination with the issuer's equity structure.

Holding 130 million yuan of bank financial products, raising 50 million yuan to supplement working capital

Suzhou Longjie plans to publicly issue no more than 29735000 shares in Shanghai Stock Exchange, and the sponsor is Guosen Securities. Suzhou Longjie plans to raise 500 million yuan, of which 396 million yuan will be used for the green composite fiber new material production project, 53.664 million yuan will be used for the high-performance special fiber research and development center project, and 50 million yuan will be used to supplement the working capital.

Suzhou Longjie is not short of money. During the reporting period, Suzhou Longjie has paid dividends for many times, with a total cumulative dividend amount of 202 million yuan.

In May 2014, after the deliberation and approval of the 2013 annual general meeting of shareholders, profits of 23.3266 million yuan were distributed to all shareholders.

In June 2015, after the deliberation and approval of the 2014 annual general meeting of shareholders, the profit of 51.9718 million yuan was distributed to all shareholders.

In June 2016, after the deliberation and approval of the 2015 annual general meeting of shareholders, a profit of 99910300 yuan was distributed to all shareholders.

In June 2017, the profit of 26.7609 million yuan was distributed to all shareholders as approved by the 2016 annual general meeting of shareholders.

Suzhou Longjie's monetary capital consists of cash, bank deposits and other monetary funds, mainly bank deposits. From 2014 to June 30, 2018, the monetary capital of Suzhou Longjie was 58.2229 million yuan, 92.3396 million yuan, 61.6374 million yuan, 158 million yuan and 72.9343 million yuan, respectively, accounting for 18.52%, 23.44%, 17.43%, 30.30% and 12.32% of current assets.

Suzhou Longjie said that at the end of 2016, the Company's monetary capital decreased compared with that at the end of 2015, mainly due to the Company's cash dividends; At the end of 2017, the Company's monetary capital increased, mainly due to the Company's profit growth and the increase of net cash inflow; At the end of June 2018, the Company's monetary capital decreased, mainly due to the increase in the amount of bank financial products purchased by the Company.

From 2015 to June 30, 2018, the amount of financial products of Suzhou Longjie Bank was 40 million yuan, 55 million yuan, 60 million yuan and 130 million yuan respectively.

Irregular capital transactions with related parties

On August 10, 2018, the CSRC released the feedback on the application documents for the IPO of Suzhou Longjie. Some inquiries are as follows:

The prospectus disclosed that during the reporting period, the issuer had entrusted the payment of loan funds through related parties. Ask the recommendation institution and the issuer's lawyer to check and make supplementary disclosure: (1) The issuer has the reason and legal compliance for entrusted payment of loan funds through related parties, whether it has been punished by relevant departments for this reason, and whether it has major violations of laws and regulations; (2) Whether the issuer's controlling shareholders and other related parties (including former related parties) require the issuer to advance wages, benefits, insurance, advertising and other period expenses for them, and whether there are costs and other expenses borne by each other; For non operating capital transactions, whether the issuer directly or indirectly provides funds to controlling shareholders and other related parties; (3) Whether the capital transactions between the issuer and its related parties comply with the provisions of relevant documents, and whether they will have a substantial impact on this issue, the recommendation agency and the issuer's lawyers are requested to express clear opinions on the independence of the issuer.

According to the application documents, the issuer accepted the freight services provided by the related party Wang Jianfang during the reporting period, and had irregular capital transactions with the related parties. Please add in the "Horizontal Competition and Connected Transactions" section of the Prospectus: (1) Explain the necessity of connected transactions, the fairness of prices, and whether there is a situation of transferring benefits through connected transactions in combination with the prices of similar transactions, the proportion of similar transactions, etc. Whether recurring related party transactions will continue to occur and whether they will affect the company's interests. (2) The reasons for the non-standard capital transactions between the issuer and related parties, and whether there are internal control defects. (3) Whether the related parties of Yang Xiaoqin, Xi Liang and others belong to the company's related parties and have been fully disclosed; Whether the disclosure of the company's related parties is comprehensive and complete, and whether there are hidden related relationships and related transactions. The recommendation institution, lawyer and accountant shall explain the verification process, method and conclusion of the issuer's related relationship and related transactions, and express clear opinions.

The sales amount of the top five customers of the Issuer in each reporting period was 232.3453 million yuan, 178.9204 million yuan, 206.6765 million yuan and 44.4998 million yuan, respectively, accounting for 17.57%, 12.49%, 17.26% and 16.03% of the operating revenue. The main customers were scattered and changed greatly. Please supplement in the "Business and Technology" section of the Prospectus: (1) Disclose the situation of customers and their corresponding income in the report period of the company according to the size and number of customer transactions, and the situation of new customers and their corresponding income in the report period; (2) According to specific business categories, sales models, etc., list the sales changes of major customers and their credit status (including but not limited to registered capital, major shareholders, main business, market position or business scale, etc.) during the reporting period, and analyze in detail the sustainability of transactions between the company and major customers in combination with industry conditions, market positions of major customers and relevant contract terms. (3) Rationality of major customers' purchase of the issuer's products, and whether there is overlap between customers and suppliers. The recommendation institution and accountant shall explain: (1) the verification process, method and conclusion of the authenticity of the customer's business, and clearly express the verification opinion, including but not limited to the method, scope and proportion of the customer's verification, the customer's business situation and whether it matches the purchase scale; (2) Whether there are abnormal customers found in the process of verification, such as whether the main customers with the characteristics of new increase, decrease and long-term large transaction amount in the report period have poor credit standing or are associated with the issuer, and whether there are associated relationships between the main customers.

According to the application documents, the purchase amount of the top five raw material suppliers in each reporting period of the issuer was 888943800 yuan, 765903800 yuan, 703466400 yuan and 189515300 yuan, respectively, accounting for 88.81%, 80.22%, 87.76% and 90.18% of the current purchase. Please supplement in the "Business and Technology" section of the Prospectus: (1) Disclose the situation of suppliers and corresponding procurement of the Company during the reporting period according to the transaction scale and quantity of suppliers, and the situation of new and reduced suppliers and corresponding procurement expenditure during the reporting period; (2) Disclose the categories of main purchases and their purchase quantities, total purchase amount and unit price changes, whether the price of specific purchase categories is significantly different from the industry index or the purchase price of companies in the same industry, and the reasons; (3) According to the specific purchase category, the main suppliers and the reasons for their changes in the reporting period, as well as the reasons for the change of the purchase proportion of a single supplier; For major suppliers with the characteristics of newly added and long-term large transaction amount in the reporting period, please make supplementary disclosure of their establishment time, sales scale, the proportion of the issuer's purchase amount in their total sales amount, and whether the price of the issuer's purchase from them has changed compared with the original suppliers. (4) How the issuer selects suppliers, how different suppliers price and market prices of main services, and whether changes in the issuer's purchase prices conform to industry trends; The relationship between the transaction scale between the company and its main suppliers in the overall business of suppliers, such as the proportion of revenue and the proportion of product types, and whether there is a business dependency relationship between the main suppliers and the issuer. The recommendation institution and the accountant shall explain the verification process, method and conclusion of the authenticity of the main supplier's business, and express clear opinions.

The prospectus disclosed that Xi Wenjie, the actual controller of the issuer, divorced his spouse in October 2014. Currently, he directly and indirectly holds about 14% of the issuer's equity, and the daughters of both parties hold about 14% of the issuer's equity; Both Xi Wenya and Xi Jianhua, close relatives of Xi Wenjie, directly or indirectly hold shares of the issuer. Xi Wenjie also signed a concerted action agreement with 11 shareholders of Longjie Investment, the controlling shareholder, to control about 41% of the equity of Longjie Investment in total. The recommendation institution and the issuer's lawyer should explain and make supplementary disclosure: (1) The reason and rationality of identifying Xi Wenjie as the actual controller only; (2) Whether the actual controller of the issuer has equity disputes with the original spouse, and whether the original spouse and her daughter have concerted action arrangements; (3) Whether the actual controller of the issuer has changed, if not, please explain the basis; (4) Please describe Xi Wenjie's actual control over the company in combination with the issuer's equity structure.

On October 23, 2018, the 159th meeting of the 17th IEC in 2018 was held. According to the announcement of audit results, the IEC raised the following questions about Suzhou Longjie:

During the reporting period, the Issuer's business performance fluctuated significantly. The representative of the issuer is requested to explain: (1) whether the reason and rationality of the sharp fluctuations in income, profit and gross profit margin are consistent with the change trend of comparable companies in the same industry; (2) The reason and rationality for the sharp fluctuation of the income, profit and gross profit margin of suede fiber products, and whether the changes in the downstream market of suede fiber will have a significant adverse impact on the performance of the issuer; (3) Analyze whether the issuer has stable profitability in combination with changes in volume and price of main products and costs, changes in upstream PET chips and PTA prices, market demand for downstream clothing and home textile products, and reasons for the withdrawal of the previous declaration. The sponsor representative is requested to explain the basis and process of verification and express clear verification opinions.

The prospectus disclosed that the issuer adheres to the chip spinning process, focuses on the research, development and production of differentiated fibers, and is technically leading in the corresponding market segments, ranking at the forefront of the industry. The representative of the issuer is requested to: (1) quote authoritative statistical data to clearly explain the industry status of the company; (2) Explain whether the issuer has sustainable core competitiveness in the field of differentiated fibers. The sponsor representative is requested to explain the basis and process of verification and express clear verification opinions.

During the reporting period, the Issuer's purchase of the top five suppliers accounted for a high proportion and the inventory balance was large. The representative of the issuer should explain: (1) the reason and rationality of the supplier concentration higher than that of comparable companies in the same industry; (2) The bargaining power between the issuer and major raw material suppliers, as well as the stability of procurement costs; (3) Whether the concentration of suppliers will have a significant adverse impact on the issuer's future sustainable profitability; (4) The balance of raw materials continued to grow, especially the reason and rationality of the substantial growth at the end of the first half of 2018; (5) The reason and rationality of the large amount of goods in stock, whether there is unsalable risk, and whether the provision for inventory depreciation is sufficient. The sponsor representative is requested to explain the basis and process of verification and express clear verification opinions.

The representative of the issuer is requested to: (1) explain whether the issuer's business and production links involve heavily polluting industries in combination with the content of regulations, business essence, production processes and processes; (2) Compare the situation of comparable companies in the same industry, and explain whether the issuer's environmental protection related expenditures in the reporting period match with its business scale, capacity and emissions; Whether the production and operation comply with the provisions of environmental protection related laws and regulations. The sponsor representative is requested to explain the basis and process of verification and express clear verification opinions.

The representative of the issuer should explain: (1) whether Longjie Limited has performed relevant legal procedures for leasing collective assets in accordance with the law, whether the rights and obligations of both parties to the lease, especially the agreement on income distribution, comply with the regulations, whether such leases are legal and compliant, and whether there are legal disputes; (2) Whether the capital source of Longjie Limited's bidding for bankruptcy assets and the capital source are legal and compliant; (3) Whether the restructuring and asset definition of Zhonggang Specialty Chemicals Factory in July 2007 are legal and compliant, and whether they comply with the terms of the lease contract; (4) Whether the relevant confirmation documents issued by the competent departments have covered the above issues. The sponsor representative is requested to explain the basis and process of verification and express clear verification opinions.

Entrusted payment of loan funds through related parties

During the reporting period, Wang Jianfang, a related party of Suzhou Longjie, and Zhangjiagang Shengji Freight Co., Ltd. under its control provided goods transportation services to Suzhou Longjie. The transaction amounts were 1310900 yuan, 709900 yuan, 1825700 yuan, 1061400 yuan and 341000 yuan, respectively, accounting for 19.06%, 10.95%, 30.04%, 19.20% and 12.94% of the current transportation costs.

At the end of each reporting period, the balance of accounts payable of Suzhou Longjie to Wang Jianfang and Zhangjiagang Shengji Freight Co., Ltd. under its control were 72700 yuan, 123700 yuan, 47600 yuan and 94500 yuan respectively.

According to the Delivery Agreement signed between the company and Shengji Freight, the freight services of both parties will continue until December 31, 2019. After expiration, the company will continue to select transportation service providers based on comprehensive evaluation of transportation price, service timeliness, service level and other factors.

Suzhou Longjie also had the situation of entrusted payment of loan funds through related parties. After the bank released the loan funds to the company's account, the company transferred the loan funds to the Longjie investment account under the supervision of the bank, and Longjie Investment re transferred the loan funds back to the company's account within a short time after receiving the funds. As of June 2017, the company has repaid all the above borrowings.

Suzhou Longjie said that because the company's payment for goods to raw material suppliers is small and repeated, the use of loans to pay for purchase and other daily business activities requires bank approval, which requires certain approval procedures and time.

In order to use bank loans conveniently and safely, after the company obtained the loan credit line as required, when using the loan funds, the company transferred the funds from the loan fund account to Longjie Investment under the supervision of the bank, and Longjie Investment promptly transferred all the funds back to the company's general settlement account after receiving them, so that the company could make small and multiple payments.

Suzhou Longjie said that after November 2016, the company used the loan funds in accordance with the regulations, and no longer entrusted the payment of loan funds with related parties. As of June 23, 2017, the loans entrusted to be paid by the company through Longjie Investment had all repaid the principal and interest in full and on time within the period agreed in the contract, and the contract had been fully performed, without causing any loss or other significant adverse effects to the relevant loan banks.

At the end of the first half of 2018, notes receivable and accounts receivable increased to 226 million

From 2015 to June 30, 2018, the total amount of notes receivable and accounts receivable of Suzhou Longjie was 54.32 million yuan, 60.0983 million yuan, 145 million yuan and 226 million yuan respectively.

From 2014 to June 30, 2018, the net accounts receivable of Suzhou Longjie were 14.7681 million yuan, 15.6254 million yuan, 11.926 million yuan, 6.0867 million yuan and 5.6032 million yuan, respectively, accounting for 4.70%, 3.97%, 3.37%, 1.17% and 0.95% of current assets.

The balances of accounts receivable of Suzhou Longjie were 15.5885 million yuan, 16.5317 million yuan, 12.8292 million yuan, 6.6313 million yuan and 6.3246 million yuan, respectively. The accounts receivable accounted for 1.17%, 1.15%, 1.06%, 0.44% and 0.78% of the current operating revenue.

The turnover rate of accounts receivable of Suzhou Longjie was 78.58 times, 89.82 times, 82.23 times, 156.59 times and 124.76 times respectively.

Suzhou Longjie said that at the end of 2017, the company's accounts receivable decreased, mainly because the sales revenue of military silk products declined, and the company gave such customers a certain credit period. The Company's accounts receivable account for a low proportion of operating revenue, and the turnover speed is fast. The balance of accounts receivable at the end of each period is basically consistent with its credit policy, and the implementation of credit policy is good.

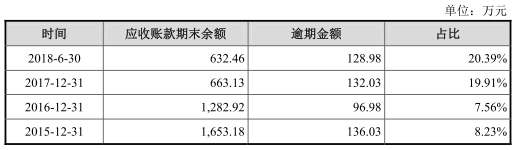

At the end of each reporting period, the overdue amount of accounts receivable of Suzhou Longjie was 1360300 yuan, 969800 yuan, 1320300 yuan and 1289800 yuan, respectively, accounting for 8.23%, 7.56%, 19.91% and 20.39% of the balance of accounts receivable. The company said that at the end of 2017, the amount and proportion of overdue accounts receivable were relatively large, mainly because some military silk customers were overdue.

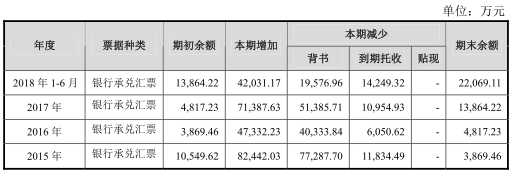

During the reporting period, the notes receivable of Suzhou Longjie were bank acceptance bills, with the amounts of 38.6946 million yuan, 48.1723 million yuan, 139 million yuan and 221 million yuan respectively.

Suzhou Longjie said that at the end of 2017 and the end of June 2018, the balance of notes receivable of the company increased, mainly because when the company sold its products, the price of products settled by customers in the form of notes was higher than that of bank transfers. Since 2017, the discount rate of bills has risen, and customers have chosen to settle their payments for goods more by notes according to the market and their own conditions.

From 2015 to January June 2018, the amount of endorsement transfer of notes receivable of Suzhou Longjie in each period was 773 million yuan, 403 million yuan, 514 million yuan and 196 million yuan respectively, accounting for 86.72%, 86.96%, 82.43% and 57.88% of the decrease in the amount of notes receivable in each period, and the amount of due collection was 118 million yuan, 60506200 yuan, 110 million yuan and 142 million yuan respectively.

Inventory turnover rate is lower than the industry average

From 2014 to June 2018, the inventory of Suzhou Longjie was 110 million yuan, 174 million yuan, 155 million yuan, 143 million yuan and 146 million yuan, respectively, accounting for 35.10%, 44.14%, 43.71%, 27.49% and 24.59% of current assets.

From 2014 to June 2018, Suzhou Longjie had a large amount of goods in stock, accounting for a high proportion of the inventory. At the end of each reporting period, the amount of goods in stock of Suzhou Longjie was 76.7925 million yuan, 122 million yuan, 124 million yuan, 106 million yuan and 95.7194 million yuan, respectively, accounting for 69.61%, 70.38%, 79.91%, 74.02% and 65.74% of the inventory. According to the prospectus, the main reason is that the company has a large variety of products. In order to ensure timely delivery, it will maintain a certain amount of inventory of goods.

According to the prospectus, the inventory turnover rates of Suzhou Longjie Company are 10.32 times/year, 8.07 times/year, 6.36 times/year, 8.43 times/year and 4.58 times/year respectively. Compared with companies in the same industry, the inventory turnover rate of the company is the same as that of Guxiandao Hailide Youfu shares are close, but significantly lower than the industry average. From 2015 to January June 2018, the average inventory turnover rate of companies in the same industry was 11.03 times/year, 8.35 times/year, 9.55 times/year, 11.50 times/year and 5.41 times/year respectively.

The gross profit rate is unstable and lower than the industry average for two consecutive years

From 2014 to January June 2018, the comprehensive gross profit margin of Suzhou Longjie was 10.90%, 20.49%, 12.92%, 16.56% and 17.08% respectively, and the gross profit margin of its main business was 10.95%, 20.51%, 12.66%, 16.50% and 17.04% respectively.

From 2015 to January June 2018, the average gross profit margin of polyester filament products of comparable companies in the same industry was 15.98%, 18.38%, 20.30% and 20.61%. The gross profit rate of Suzhou Longjie's main business in 2015 was higher than the average of the industry, and the gross profit rate of its main business in 2016, 2017 and January June 2018 was lower than the average of the industry.

Suzhou Longjie said that in 2016, the gross profit margin of the company's main business declined, mainly due to the decline of the fashion trend of suede fabrics and clothing, the large inventory of downstream fabric manufacturers at the end of 2015 and the increase in supply and other comprehensive factors. The prices of suede fiber products declined, and their gross profit margin declined.

In 2017, the gross profit rate of the company's main business increased, mainly due to the strong market demand for rabbit like wool, wool and other high imitation/super imitation fur fibers and PTT fibers with high gross profit rate launched by the company in recent years, their sales revenue and proportion increased, and the gross profit rate of suede like fiber series and other products rebounded.

From January to June 2018, the gross profit margin of the company's main business increased, mainly due to the strong market demand for PTT fiber, its sales revenue and proportion increased, and the gross profit margin of other types of products increased.

In 2016, the price of suede fiber series products dropped 23.70%

From 2015 to January June 2018, the sales revenue of Suzhou Longjie suede fiber series was 686 million yuan, 533 million yuan, 519 million yuan and 294 million yuan, respectively, accounting for 47.91%, 44.49%, 34.67% and 37.05% of the sales revenue.

In 2016, the sales price of Suzhou Longjie suede fiber series products dropped by 23.70%. From 2015 to January June 2018, the sales prices of suede fiber series products were 13800 yuan/ton, 10500 yuan/ton, 12600 yuan/ton and 13300 yuan/ton respectively.

Suzhou Longjie said that in 2016, the sales price of suede fiber series products decreased by 23.70% compared with 2015, mainly because the fashion trend of suede fabric clothing began to fade from the fourth quarter of 2015, downstream fabric manufacturers had more inventory at the end of 2015, the demand for suede fiber decreased, and the market supply of this product increased.

Asset liability ratio decreases year by year

From 2014 to June 2018, the total liabilities of Suzhou Longjie were 304 million yuan, 232 million yuan, 191 million yuan, 201 million yuan and 175 million yuan respectively.

Among them, short-term borrowings were 180 million yuan, 95 million yuan, 65 million yuan, 45 million yuan and 0 yuan, respectively, accounting for 69.34%, 47.78%, 38.59%, 23.71% and 0% of current liabilities.

The notes payable and accounts payable of Suzhou Longjie were 37.2393 million yuan, 57.7059 million yuan, 31.7496 million yuan, 76.2854 million yuan and 80.7755 million yuan respectively.

Suzhou Longjie said that at the end of 2017 and the end of June 2018, the amount of notes payable of the company was relatively large, mainly because the company cooperated with Zhangjiagang Branch of Zhejiang Merchants Bank Co., Ltd. in bill pledge business, and issued notes payable under the pledge of notes receivable. The number of notes payable issued increased, and the endorsement of notes receivable decreased accordingly.

At the end of each reporting period, the asset liability ratio of Suzhou Longjie was 41.00%, 29.24%, 26.61%, 24.07% and 19.79%, respectively. The asset liability ratio declined and was lower than the average of the industry, with strong solvency. From 2015 to June 30, 2018, the average asset liability ratio of companies in the industry was 51.45%, 47.16%, 46.67% and 43.49%, respectively.

8 properties and 3 land use rights were mortgaged

Suzhou Longjie has secured 8 houses and buildings with property right certificates, which are located in Zhangjiagang Provincial Development Zone (No. 19, Zhenxing Road), Yangshe Town, with a total area of 161628.05 square meters.

Suzhou Longjie has 3 land use rights, all of which have been mortgaged, located in Zhangjiagang Provincial Development Zone (No. 19, Zhenxing Road), with a total area of 155207.20 square meters and a net book value of 21.4861 million yuan.

The first land use right mentioned above was registered as land mortgage on May 14, 2018 Industrial and Commercial Bank of China The maximum amount mortgage contract signed by Zhangjiagang Branch of the Joint Stock Company Limited, Shazhou (Di) Zi No. 0091 in 2018, provides the maximum amount of guarantee liability of RMB 146 million.

The above second land use right was registered as land mortgage on April 26, 2016, which is the Maximum Mortgage Guarantee Contract signed by Suzhou Longjie with Jiangsu Zhangjiagang Rural Commercial Bank Co., Ltd., and the maximum amount of guarantee liability is 64107800 yuan.

The third land use right mentioned above was registered as land mortgage on September 29, 2015, which was jointly signed by Suzhou Longjie and China bank for economic construction The maximum amount mortgage contract signed by Suzhou Zhangjiagang (Suzhou Longjie) 2015 ROR 001 No. 02 signed by Zhangjiagang Branch of the joint-stock company limited, the maximum amount of guarantee liability provided is 76.712 million yuan.

The proportion of shares held by the former wife of the actual controller is high

According to the Daily Economic News, there are many stories about the control of Suzhou Longjie.

In the prospectus (application draft) submitted by Suzhou Longjie in 2017, it was mentioned that the controlling shareholder of Suzhou Longjie was Longjie Investment. Among the shareholders of Longjie Investment, Yang Xiaoqin, a natural person shareholder with the highest shareholding ratio, is 15.13%, while she also has a direct shareholding ratio of 4.48% in Suzhou Longjie Investment. The total direct and indirect shareholding ratio can reach 14.93%, which is the natural person shareholder with the highest shareholding ratio.

However, the actual controller of Suzhou Longjie disclosed at that time was Xi Wenjie, Yang Xiaoqin's ex husband. The reason is that although the total proportion of indirect and direct shares held by individuals is lower than that of Yang Xiaoqin, he signed a concerted action agreement with 11 shareholders of Longjie Investment, controlling about 41% of the equity of Longjie Investment in total, so he can control Longjie Investment, thus controlling Suzhou Longjie.

As for this, in the feedback of the CSRC on August 10 this year, the company was required to make supplementary disclosure on this situation. The reason and rationality of Xi Wenjie as the actual controller, and the actual control ability of Xi Wenjie was explained on the equity structure. In addition, it is required to disclose whether Xi Wenjie and his ex-wife Yang Xiaoqin have equity disputes.

In this regard, in the latest prospectus, the actual controller of Suzhou Longjie became "Xi Wenjie and his daughter Xi Liang". In addition, Xi Wenjie also signed the Agreement of Concerted Action with 11 shareholders. Finally, Xi Wenjie and Xi Liang jointly controlled 85.38% of the voting rights of Suzhou Longjie.

The change of actual controller of Suzhou Longjie is shown in the first prospectus (photo source: the prospectus submitted by the company in 2017)

The change of actual controller of Suzhou Longjie is shown in the second prospectus (photo source: the prospectus submitted by the company in 2018)

In the latest prospectus, Yang Xiaoqin, a single natural person with the highest proportion of shares in total, is no longer as good as the current controllers, the Xi Family's father and daughter, let alone those who act in concert. And will having such a high number of ex-wife shareholders in the company have an impact on control?

Suzhou Longjie mentioned in the latest prospectus: First of all, there is no concerted action arrangement between Yang Xiaoqin, Xi Liang and other shareholders of the company, and there is no control over the shareholders' meeting of the company, and there is no control over Suzhou Longjie's controlling shareholder Zhangjiagang Longjie Investment Co., Ltd; In addition, Yang Xiaoqin has never served as a director or senior manager of the company since the establishment of Suzhou Longjie, and has never participated in major decisions of the company. At the level of the board of directors and operation management of the company, Yang Xiaoqin has no control, does not exert any influence on the company's business decisions, and it is reasonable not to identify Yang Xiaoqin as the actual controller or joint actual controller.

The first customer is Lao Lai

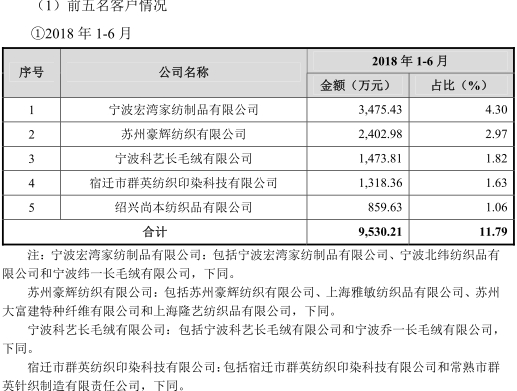

According to Phoenix. com, Ningbo Hongwan Home Textile Products Co., Ltd. is the largest customer of Suzhou Longjie, and also the second largest bill receivable customer. In the first half of this year, Longjie sold 34.7553 million yuan of goods to Ningbo Hongwan, accounting for 4.3% of the company's total sales.

Ningbo Hongwan actually includes three companies, namely Ningbo Hongwan Home Textile Products Co., Ltd., Ningbo Beiwei Textile Co., Ltd., and Ningbo Weiyi Long Wool Co., Ltd.

According to Tianyan's data, Ningbo Beiwei Textile Co., Ltd. was publicized as a dishonest company by the Supreme People's Court, and was sentenced to pay 7.1941 million yuan of execution fee and interest, bear 63370.55 yuan of execution fee, pay 8 million yuan of loan and interest, and advance principal of 2.7728 million yuan and interest. In addition, according to the information query of the people subjected to enforcement by the national courts, the Cixi People's Court enforced the assets of Ningbo Beiwei Textile Co., Ltd. of 68 million yuan.

Beiwei once talked about environmental protection in an interview with Textile and Garment Weekly in 2013, claiming to spend 16 million yuan to introduce new technologies, achieve zero sewage discharge and wastewater reuse, and achieve the goal of energy conservation and emission reduction of 50%. "Our production capacity is expanding, but the amount of sewage discharge is not increasing at all. The company's reclaimed water reuse project is about to start. After starting, 75% of the wastewater can be recycled... to ensure zero discharge of enterprise sewage."

However, the environmental protection of Beiwei Company was on the red light that year. According to the evaluation results of enterprise environmental behavior credit rating in 2013 released by Ningbo Environmental Protection Bureau, 39 of the 606 enterprises that participated in the evaluation of enterprise environmental behavior credit rating were rated as bad environmental protection enterprises (red card), including Beiwei Company.

According to the annual report released by Ningbo Hongwan, the company paid social insurance to only one employee in 2016, and only 20 employees in 2017. As the largest customer of Longjie Shares, the public channel could not find any business disputes in Ningbo Hongwan.

It is reported that there was once an administrator surnamed Pan in Hongwan, Ningbo, who was also an employee of Ningbo Beiwei plush company. Yu Wanjun, the chairman of the board of Beiwei plush company, also served as the chairman of Beiwei textile company, which was also the Lai Lai announced by the Supreme Law.

Yu Wanjun and Long Jie Chairman Xi Wenjie are members of the China Wool Textile Industry Association, and have successively served as the executive deputy directors of the second and third artificial fur professional committees.

There is no obvious advantage in the field of PTT for projects invested by raised funds

According to the Investment Times, PTT fiber was first commercialized by Shell in 1998, and DuPont subsequently produced PTT fiber and launched its fiber product brand SORONA. As the best alternative to traditional petroleum based fiber, PTT fiber has also received strong support from the Chinese government. However, limited by technological development, only the production processes of Tsinghua University and East China University of Science and Technology have realized the industrial production of key raw materials for PTT fiber.

Chinese Chemistry According to the latest report of the Fiber Industry Association, China carried out research on PTT fiber and its core raw materials in the late 1990s. At present, the contract market size of PTT fiber has reached 90000 tons, and the main suppliers include Suzhou Longjie, Jiali High Fiber, Zhongba Technology (Shenghong Group), Meijingrong, and foreign manufacturers such as Xiaoxing Chemical Fiber and Invista.

Among them, Suzhou Longjie's PTT fiber series products achieved sales revenue of 64.1336 million yuan and 81.3778 million yuan respectively in 2015 and 2016, accounting for 4.48% and 6.79% of the total revenue respectively. This situation has changed slightly since 2017. In the same year, its PTT fiber sales reached 176 million yuan, accounting for 11.74%, while in the first half of 2018 alone, it reached 117 million yuan, accounting for 14.81%. During the reporting period, the gross profit rate of PTT fiber was 22.97%, 23.58%, 23.40% and 25.42% respectively, showing an upward trend, and was significantly higher than that of deer skin fiber and leather fiber.

From the perspective of the whole PTT fiber industry, the sales volume of Suzhou Longjie in 2017 was 7582.62 tons, accounting for about 8% of the market share.

The introduction of Suzhou Longjie raised investment project shows that of the nearly 500 million yuan raised this time, 397 million yuan will be used for the "green composite fiber new material production project", which will increase the production capacity of 50000 tons/year polyester fiber filament, mainly PTT fiber and composite fiber.

However, Suzhou Longjie does not have obvious advantages in terms of the length of its entry into the PTT fiber field and its technical reserves. The prospectus shows that the company has 63 patents and 4 trademarks, but most of these patents are related to the previous key product series, and only 3 patents are related to the PTT fiber series.

As the representative of new polyester fiber industry, PTT fiber has been vigorously supported. Many enterprises have begun to increase investment and expand production lines. At the beginning of 2017, Meimeirong Chemical Industry Co., Ltd., located in Zhangjiagang with Suzhou Longjie, announced to launch the project of "200000 t/a PTT polymerization and spinning integration". The company claims to have conquered the key technology of biological 1,3-propanediol, realized the biological manufacturing of the above key raw materials, and realized the industrial large-scale production. If domestic companies make technological breakthroughs in core raw materials and expand to the PTT fiber industry, it will bring some pressure on the price and capacity scale of related enterprises, including Suzhou Longjie.

Is there a risk of forced elimination of product processes?

According to Global Network, the average selling price of Suzhou Longjie's fiber products is far higher than that of other listed companies in the same industry. The explanation given in this prospectus is that "products produced by different production processes are different", that is, the chip spinning process adopted by Suzhou Longjie can produce products with high technology content, multiple functional requirements and complex structure.

But I'm afraid this explanation is hard to stand on. According to people in the chemical industry, there is little difference in the performance of the final products, whether melt direct spinning or chip spinning. On this basis, the terminal product price of Suzhou Longjie is 20%~40% higher than that of other companies with more scale advantages in the same industry, which is lack of industry rationality.

What's more, the "chip spinning process" adopted by Suzhou Longjie is also a "backward technology" with high energy consumption, and the risk of forced elimination is extremely high in the future.

One of the representative companies in the same industry announced by Suzhou Longjie is Xinfengming. In its prospectus, Xinfengming disclosed that in recent years, "the operating rate of enterprises adopting chip spinning process has differentiated from that of enterprises adopting melt direct spinning process", and "chip spinning process has high energy consumption, production stability is lower than that of melt direct spinning process, and melt direct spinning process has gradually replaced chip spinning process" "According to the statistics of China Chemical Fiber Industry Association, in 2015, the average operating rate of polyester filament production enterprises adopting melt direct spinning process was 76.8%, and the average operating rate of polyester filament production enterprises adopting chip spinning process was only 34.1%

From the information disclosed by Xin Fengming, the "chip spinning process" adopted by Suzhou Longjie is obviously not as excellent as the company itself claims, which makes it questionable that Suzhou Longjie has false statements about melt direct spinning and the chip spinning process it adopts.

In addition, according to the prospectus of Xinfengming, "Xinfengming Chemical Fiber was originally a subsidiary of Xinfengming that produced polyester filament by chip spinning, and its business premises were located in the above implementation scope. In response to the government's development strategy of improving the urban environment, optimizing the industrial structure, and accelerating economic transformation and upgrading, Xinfengming Chemical Fiber stopped the original polyester filament business". Under the environment of increasingly strict environmental protection inspection and limited energy consumption industry, will Suzhou Longjie, which uses the chip spinning process, face the risk of forced elimination in the future?

Editor in charge: Chen Youran SF104