The 21st Century Economic Reporter Li Yuan reports from Beijing

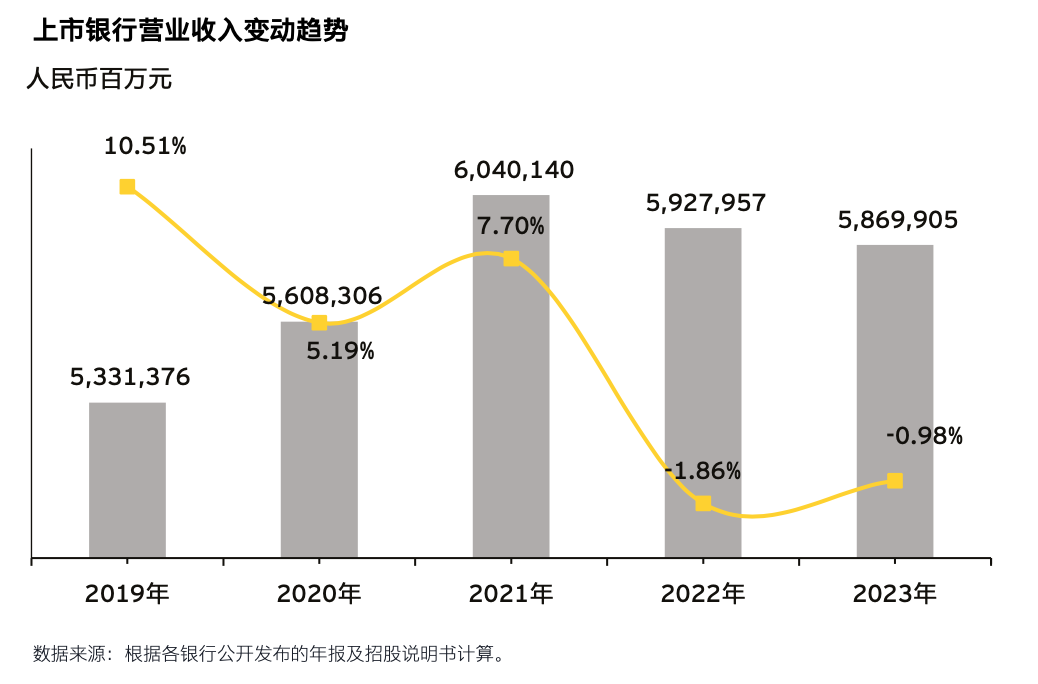

On May 14, Ernst&Young released the Review and Future Outlook of China's Listed Banks in 2023 (the analysis object is 58 A+H listed banks) and the First Quarter Performance Overview of China's 42 A-share listed banks in 2024, which is the 17th year that Ernst&Young released the report. The report shows that 58 listed banks will achieve an operating income of 5869.905 billion yuan in 2023, with a growth rate of - 0.89%, and - 1.86% in 2022, which is the second consecutive year of negative growth, of which the net interest income is the first negative growth since 2017, and the net income of fees and commissions is the second consecutive year of negative growth; Net profit was 2169047 million yuan, with a growth rate of 1.43%, down 5.77 percentage points from 7.20% in 2022.

The report shows that 42 A-share listed banks achieved an operating income of 1472.655 billion yuan in the first quarter of this year, down 1.73% year on year and up 1.79 percentage points from 2023; Net profit was 578.127 billion yuan, down 0.81% year on year, 4.03 percentage points lower than the growth rate in the first quarter of 2023, the first negative growth since at least 2019 (according to historical reports).

"In the face of severe and complex business environment, domestic listed banks actively face changes, adhere to the same frequency resonance with the real economy, adhere to the concept of financial goodness, focus on the 'five major articles' of finance, improve operation and management efficiency, operate prudently, coordinate development and safety, and make progress in stability, so as to cross the cycle and achieve the long-term goal of high-quality development." Said Xin Yi, chief partner of Ernst&Young Greater China Financial Services.

For example, the report shows that listed banks respond with "intelligence" and accelerate the transformation of digital intelligence. 27 listed banks disclosed the number of financial technology/information technology personnel in their annual reports, and the total number of related technology personnel exceeded 144200. According to the data of 25 listed banks that have disclosed the number of financial technology personnel in the last three years, the proportion of technology personnel continues to rise, from 5.04% in 2021 to 5.98% in 2023.

Jiang Changzheng, the partner in charge of financial services audit in Ernst&Young China North, said that the current digital intelligence capability has become the core competitiveness of listed banks, and the exploration and practice of large model technology will further innovate the existing product services, business processes, operation methods and even business models, bringing new opportunities for the transformation of the banking industry. "Although the big model has a broad application prospect in the banking field, it also faces some challenges in the actual implementation process, such as data privacy and security, model interpretability, accuracy of prediction, and ethical and legal protection."

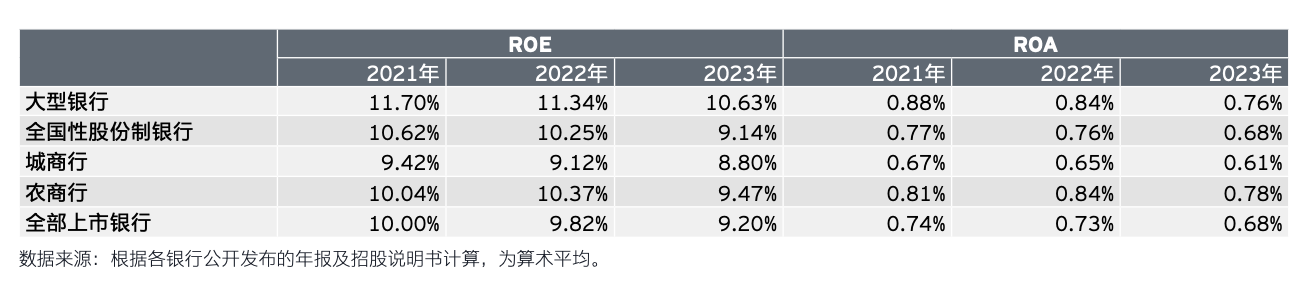

In 2023, the profit efficiency of listed banks declined slightly, and the average return on equity ("ROE") was 9.20%, 0.62 percentage points lower than 9.82% in 2022; The average return on total assets ("ROA") was 0.68%, down 0.05 percentage points from 0.73% in 2022. The average ROE of large banks, joint-stock banks, urban commercial banks and agricultural commercial banks decreased by 0.71, 1.11, 0.32 and 0.90 percentage points respectively; The average ROA of large banks, joint-stock banks, urban commercial banks and rural commercial banks decreased by 0.08, 0.08, 0.04 and 0.06 percentage points respectively.

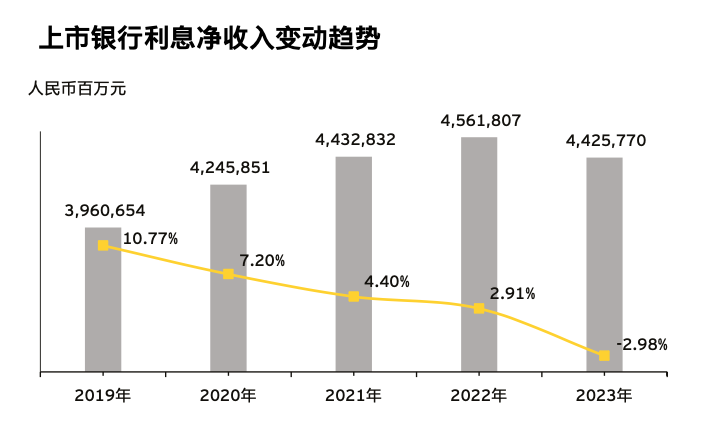

The report shows that the total net interest income of listed banks in 2023 is 4425.77 billion yuan, down 2.98% year on year, and the growth rate is 5.89 percentage points lower than 2.91% in 2022. "The decrease in net interest income was mainly affected by the narrowing of net interest margin (net interest yield). The average net interest margin of listed banks in 2023 was 1.69%, down 25 basis points from 2022." The report said.

Specifically, the net interest income of large banks decreased by 2.54% year on year and increased by 3.59% year on year in 2022; The joint-stock banks decreased by 4.94% year on year and increased by 0.41% year on year in 2022, except Industrial Bank and Zheshang Bank Except for the 0.85% and 0.99% increase in net interest income, the net interest income of other joint-stock banks decreased year on year; Urban commercial banks decreased by 0.47% year on year, and increased by 5.45% year on year in 2022; Rural commercial banks decreased by 4.70% year on year and 1.69% year on year in 2022. With the exception of Changshu Rural Commercial Bank, which increased by 11.69%, the net interest income of other rural commercial banks decreased, including Jiutai Rural Commercial Bank and Guangzhou Rural Commercial Bank, which decreased by more than 10%, and the decline of other rural commercial banks was less than 8%.

The report shows that the proportion of net income from commission and commission of listed banks has been declining in the past three years, which will be 14.28%, 14.19% and 13.18% respectively from 2021 to 2023. In 2023, the net income of handling fees and commissions will be 773.406 billion yuan, down 8.05% year on year. "In 2023, in order to support the development of the real economy, listed banks will continue to take measures to reduce fees and yield profits to customers, and due to the fluctuation of the capital market, the income from handling fees such as wealth management services and advisory services will decline, resulting in a decline in the net income from handling fees and commissions," the report said.

Specifically, the net income of service charges and commissions of 11 banks increased compared with 2022, and that of 47 banks decreased compared with 2022. The net income of handling charges and commissions of large banks decreased by 2.01%, 0.25 percentage points lower than 2.26% in 2022, of which Industrial and Commercial Bank of China 7.71%; The net income of service charges and commissions of joint-stock banks decreased by 14.51%, 12.69 percentage points more than 1.82% in 2022, of which Industrial Bank decreased by 38.38%, mainly due to the increase in the base of one-time income recognition of old wealth management products in 2022; The net income of commission and commission of urban commercial banks decreased by 23.73%, 17.49 percentage points higher than 6.24% in 2022, of which Bank of Beijing 、 Bank of Chongqing The net income of commission and commission of Shengjing Bank decreased by 46.90%, 45.99% and 44.32% respectively.

By the end of 2023, the total liabilities of listed banks had totaled 270475.036 billion yuan, an increase of 27603.319 billion yuan, or 11.37%, compared with the end of 2022, and the growth rate had dropped 0.34 percentage points. The debt structure is relatively stable, and the highest proportion of deposits in debt is the main driving factor for debt growth. The proportion of interbank debt declined, the proportion of debt issued bonds declined, and the proportion of other liabilities rose.

In terms of deposits, by the end of 2023, the balance of deposits in listed banks had totaled 201810.043 billion yuan, an increase of 19380.350 billion yuan, 10.62%, or 1.82 percentage points lower than the end of 2022. Among them, the deposit growth rates of large banks, joint-stock banks, urban commercial banks and agricultural commercial banks were 12.09%, 6.43%, 10.40% and 8.17% respectively.

By the end of 2023, deposits accounted for 74.61% of total liabilities, down 0.50 percentage points from 2022. The proportion of deposits of different types of listed banks varies greatly, reflecting the different deposit absorption capacities of different types of banks and their different dependence on deposits. By the end of 2023, deposits of large banks, joint-stock banks, urban commercial banks, and agricultural commercial banks accounted for 79.49%, 65.11%, 66.17%, and 78.39% of total liabilities, respectively.

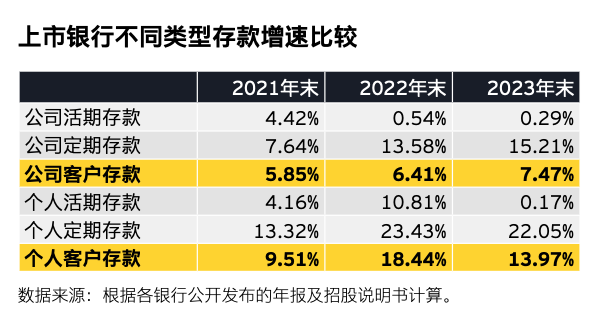

The report shows that in 2023, the trend of deposit periodization of listed banks will become increasingly obvious. By the end of 2023, the proportion of time deposits of listed banks was 57.60%, up 4.08 percentage points from the end of 2022, and the trend of fixed deposits continued to rise.

Specifically, the proportion of time deposits of large banks was 57.25%, up 5.00 percentage points from the end of 2022, of which Postal Savings Bank The proportion is the highest, 71.12%, up 3.46 percentage points from the end of 2022; The proportion of fixed deposits in joint-stock banks was 55.42%, up 1.52 percentage points from the end of 2022, of which Minsheng Bank The proportion was the highest, 67.88%, up 1.65 percentage points from the end of 2022, China Merchants Bank The proportion is the lowest, 44.67%, 7.92 percentage points higher than that at the end of 2022. It is the only joint-stock bank in which the proportion of demand deposits is higher than that of fixed deposits; The proportion of fixed deposits of urban commercial banks was 62.33%, up 3.35 percentage points from the end of 2022, of which the proportion of Harbin Bank was the highest 77.05%, up 1.32 percentage points from the end of 2022; The proportion of fixed deposits of Rural Commercial Bank was 65.38%, up 3.75 percentage points from the end of 2022, of which the proportion of Jiutai Rural Commercial Bank was the highest 76.82%, up 5.40 percentage points from the end of 2022.

From the perspective of deposit types, in 2023, the balance of personal deposits of listed banks will increase by 13.97%, down 4.47 percentage points from the end of last year, and the growth rate of personal deposits will be 6.50 percentage points higher than that of public deposits.

Against the background of slowing macroeconomic growth and increasing volatility in the capital market, the willingness of corporate residents to invest and consume has declined. At the same time, affected by the increased fluctuation in the net value of wealth management products, the deposit growth of listed banks is fast, and the trend of deposit periodization is obvious, which brings pressure on the cost control of listed banks. "Listed banks need to continue to strengthen debt quality management, do a good job in forward-looking evaluation of prices, and dynamically adjust coping strategies from the perspective of debt structure, stability, cost and asset matching," the report said.

From the perspective of loan structure, by the end of 2023, retail loans of listed banks accounted for 36.62% of the total loans, down 2.06 percentage points from the end of the previous year, and their proportion in the total loans further declined. Among them, retail loans of large banks accounted for 35.92% of the total loans, retail loans of joint-stock banks accounted for 41.62% of the total loans, and retail loans of urban commercial banks and rural commercial banks accounted for 30.47% and 31.93% of the total loans, respectively. Changshu Rural Commercial Bank Ping An Bank The retail loans of Postal Savings Bank and China Merchants Bank accounted for more than 50% of the total loans.

Massive information, accurate interpretation, all in Sina Finance APP

Editor in charge: Zhang Wen