"One day when I was bored, I checked my own credit investigation, and found that there was an extra credit loan, but I didn't have a credit loan, so why did a loan record appear? Later, I went back to check the bill and found that there was a problem with an order on Ctrip." Recently, Xiao Chen (not his real name) from Nanjing, Jiangsu Province told Zhongxin Jingwei.

Careful netizens can easily find that nowadays, the borrowing function has penetrated almost every commonly used app, and these apps are also "reminding" you that you can borrow money in various ways.

Although this can improve the convenience of consumption to a certain extent, it also has some hidden dangers. Many consumers are also troubled by problems such as forgetting to repay the loan after opening the loan, high loan interest rate, and leakage of personal information.

"Why is there an extra loan in the credit investigation?"

Xiao Chen recalled that in July 2022, when he booked a hotel with Ctrip, he was pushed by the app to "pay after staying". The service said that you can check in directly without paying in advance. "After checking in, I found that this was actually a credit loan."

He believes that in the whole process of payment opening, Ctrip did not prompt consumers to read the relevant agreement in an obvious place, and the service name has an inductive tendency, so it is difficult for consumers to find the nature of their loans.

"People who are not familiar with financial rules are likely to open this' official recommendation ', which will generate a small loan service." Xiao Chen said that he immediately closed the order after he found something wrong, and subsequently did not continue to use this function on Ctrip.

It was not until the eve of graduation in July 2023 that Xiao Chen found this loan record when he inquired about personal credit, and then he complained to Ctrip customer service, hoping to eliminate this loan record on personal credit.

The loan record on Xiao Chen's personal credit investigation provided by the interviewee

"The customer service replied that they would help to verify the problem, but no staff member continued to call me later to solve the problem, so I complained in Black Cat [Complaint Entrance] To make a complaint. " Xiao Chen said that he also consulted the People's Bank of China, and the staff told him that he would automatically clean up the micro loan records in five years.

Xiao Ling (a pseudonym) of Yuncheng, Shanxi, also had a similar experience. Xiao Ling recalled that on July 11, 2023, she bought tickets for her family on Qunar.com App. She checked the ticket change and refund package because she was worried that her family could not get on time.

After the payment is successful, Xiaoling's mobile phone receives the SMS notification of opening the "take it to spend" loan service. "I chose to pay by credit card according to the normal payment process, but somehow, I opened it and took it to spend," Xiao Ling said.

Xiaoling received the "take it to spend" payment SMS provided by the respondent

"Because of the nature of my work, I can't use online loans, and the company even checks credit card payments very strictly, I pay special attention to these." After finding the problem, Xiao Ling was very angry about being opened online loans for no reason.

Later, she contacted Qunar.com customer service and asked the customer to close the order, reuse other payment methods, and request the other party to modify the payment settings. However, the customer service told Xiao Ling that the service was opened by her authorization, and the platform could not be opened by force. After Xiao Ling returned the order, the customer service did not call to solve the problem.

After searching the Internet, Xiao Ling found that her experience is not an exception. She hopes to strengthen the supervision of the platform and introduce relevant regulatory measures to safeguard the rights and interests of consumers.

According to Ctrip App, "Take Flower" is a consumer credit product provided by Chongqing Ctrip Micro Loan Co., Ltd. (hereinafter referred to as "Ctrip Micro Loan"). Credit purchase is a credit consumption service provided to individuals by institutions with legal financial business qualifications such as Ctrip Financial United Bank and consumer finance companies. It is currently supported on platforms such as Ctrip and Qunar.

On July 25, 2023, the brand of Narwha was upgraded to "Narwha credit purchase". The page shows that the purpose of this renaming is to better implement the regulatory requirements, make users more clearly understand the product use attributes, and avoid brand confusion.

On the 7th, the reporter verified the above complaints with Ctrip and Qunar.com respectively. Since the two complainants were unwilling to disclose their personal order information to the platform party, the platform party said it was unable to verify the relevant information.

Not only travel apps, but also takeaway, taxi and even office software in daily life are all interested in the loan business. In 2021, Li Feng (not his real name) in Zaozhuang, Shandong Province, was attracted by the loan advertisement on WPS Office software due to lack of funds, so he downloaded Jinshan Financial App loans, totaling 6, totaling 74800 yuan. As of March 2023, a total of 55848.21 yuan had been repaid.

A personal consumption loan contract provided by Li Feng shows that the loan amount is 50000 yuan, the loan interest rate (simple interest) is one year LPR 3.85%+3.55% (i.e. 7.4%/year), the repayment method is installment, and the lender is Fujian Huatong Bank. However, after paying off the eight phase loan, Li Feng believed that the actual loan interest rate of this loan was far higher than 7.4%, even reaching 36%.

According to the repayment record provided by Mr. Li, he repays 5027.15 yuan every month. If he repays for 12 months, the actual repayment amount is 60325 yuan, and the annualized interest rate calculated by IRR is about 36%. Li Feng said that he hoped to negotiate to reduce the loan interest rate. However, when communicating with the customer service in early 2022, the other party's attitude was not good. At present, he is still waiting for the solution provided by the other party.

At present, Sino Singapore Jingwei has failed to search Jinshan Financial App in multiple Android app stores and Apple app stores. Tianyan App shows that the main body of the brand is Wuhan Jinshan Microfinance Co., Ltd. On the 6th and 7th, the reporter called the company's industrial and commercial registration telephone to verify, but no one answered. Kingsoft Office Relevant people said that Kingsoft Finance was not a product of Kingsoft Office and could not answer relevant questions.

The end of the Internet is lending?

The reporter actually found that in many "My" or "My Wallet" columns of the App, there is a "borrow" entrance, and some of them also have red letters above the loan amount indicating "cash withdrawal", "interest free 90 days" and "high limit".

For example, when the reporter opened the halo bike, he could see a red envelope with the words "receive the limit" on the home page. After clicking on it, the pop-up window on the page prompted "1 coupon you still need to use". After clicking to check, he found that there was an interest free coupon of 20 yuan for new customers. The return page is the loan page. There are also some video apps that attract users to obtain credit lines by giving free video members for one month.

Source: Halo Bike App

Source: Halo Bike App Source: iQIYI App

Source: iQIYI App The "Borrow Money" portal often only reminds consumers that they can borrow money from the App, and many other apps are designed as "default recommendations" during the final payment phase of consumers.

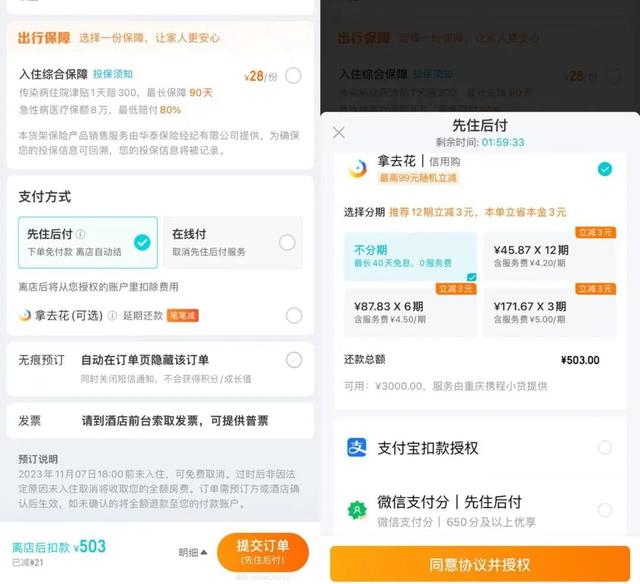

The reporter tried to use Qunar App to book a hotel. On the order submission page, he found that "pay after stay" was checked by default in the payment method column. After clicking the exclamation mark above, he displayed a common question, which explained that "pay after stay" was a service provided by Qunar for users with high credit. After leaving the store, he would deduct money from the authorized account when the consumer placed the order.

However, the reporter found that if the "stay first and pay later" service is selected, when choosing the payment method, the "take away spend" credit purchase is still in the front position. If you choose Alipay or WeChat payment, the page will display "recommend using" take away spend "credit purchase, official credit payment", and click "agree to the agreement and authorize" below to enter the password, The agreement does not require consumers to read it.

In contrast, some bank apps require customers to manually click Confirm to read the agreement when they handle business. The time for reading the agreement is more than 5 seconds, or fill in the statement of the agreement that has been read. Otherwise, they cannot click Next to operate.

Source: Qunar App

Source: Qunar App In addition, the reporter noticed that only by dragging down the page to the end can we see two agreements - the Agreement on Withholding Service and the Agreement on Purchasing with Credit. The second agreement contains a copy of "Take it to spend - Chongqing Ctrip Small Loan Contract", which shows that Party A's loan is Chongqing Ctrip Micro Loan Co., Ltd., and the purpose of the loan is to purchase on the platform. The annual comprehensive effective interest rate of the loan does not exceed 24%. In addition, the default interest is calculated on a daily basis, with a daily interest rate of 0.065% and an annualized interest rate of 23.4% (simple interest).

The above contract also includes in the statement that the borrower of Party B agrees that Party A will provide the information related to this contract and other information of Party B to other legally established credit institutions such as the Internet Finance Association of China, the People's Bank of China Credit Reference Center in accordance with relevant laws, regulations and regulatory provisions.

Internet companies should pay attention to legal compliance

After sorting out, China Singapore Jingwei found that some Internet companies have set up special micro loan companies to operate small loan businesses, such as Chongqing Meituan Sankuai Micro Loan Co., Ltd. under Meituan and Chongqing Ctrip Micro Loan Co., Ltd. under Ctrip. At the same time, Internet companies will also cooperate with other licensed financial institutions, such as banks and consumer finance companies to lend. Some platform companies did not set up small loan companies, but only channeled financial institutions.

According to Black Cat complaints, the problems complained by users include credit investigation, high loan interest rate, violent collection, information leakage, etc.

Why do Internet companies like loan business? Dong Ximiao, the chief researcher of China Merchants Association, said to Sino Singapore Jingwei that this is an important way for Internet companies to realize their traffic and customers. These platforms have accumulated a large number of customers, and their normal operations will also attract a lot of traffic. It is understandable that they can realize the loan business and obtain more benefits, but they should pay attention to legal compliance issues.

From the interest rate displayed on these platforms, it is usually between 7.2% and 24%. At present, the annualized interest rate of consumer loan products of many banks is below 4%. On the issue of interest rates, Dong Ximiao pointed out that financial institutions and small loan companies are not subject to the LPR 4 times ceiling, but he called on financial institutions to gradually reduce their loan interest rates, which should not be too high.

As for whether the credit investigation on micro lending will affect the future housing loan, a personal loan manager of a state-owned bank said to Zhongxin Jingwei that it has an impact. He was worried that the customer's down payment was all borrowed, and he would ask the customer to repay before applying for the loan. If the average consumption of credit card and other consumer loans in the past six months is tens of thousands, the bank will have doubts. Generally, a small loan of several hundred yuan has little impact.

Another personal loan manager of a joint-stock bank also said that it would have an impact, and the core concern was that consumer loan funds would be used to buy houses. In addition, the interest rate of small loans is much higher, and the bank will question the repayment ability of customers. However, as long as the loan is paid off before, it generally does not affect.

Dong Ximiao believes that the Internet platform should pay attention to several issues when carrying out lending business or channeling lending business: first, it should fully, comprehensively and truthfully inform relevant information, where the information will be used after clicking authorization, by which institution the loan is provided, what the loan interest rate is, and whether there are other fees, it should be fully and truthfully informed; The second is to be qualified. Access to customer information should be minimized. One click authorization is not allowed. All user information should be taken away, which may lay hidden dangers for future brutal collection.

Dong Ximiao suggested that ordinary financial consumers need to borrow money and try to find formal financial institutions. If you are on the Internet platform, you should find a reliable big Internet platform. At the same time, it is necessary to see clearly who provides the loan, what the loan interest rate is, whether it is an annual interest rate, a monthly interest rate or a daily interest rate, and whether there are any other fees in addition to the loan interest.

In addition, Dong Ximiao suggested that financial consumers should keep their debt level within a reasonable limit. For consumer credit products, financial consumers, especially young people, should apply as needed and act within their capabilities. They should not borrow blindly. Generally speaking, the monthly loan payment should not exceed half of the household income. Financial services are not always better as they sink. Financial institutions and Internet platforms should take measures to effectively prevent excessive sinking, excessive credit and other problems such as "not lending" and "excessive lending", so as to further reduce the probability of "co debt risk".

Massive information, accurate interpretation, all in Sina Finance APP

Editor in charge: Zhang Wen