More and more provinces are realizing the pension increase in 2022.

On July 19, Hainan and Shandong successively issued the Notice on Adjusting the Basic Pension of Retirees in 2022 to continue to increase the pension of retirees. According to combing, so far, At least 22 provinces in China have defined relevant adjustment plans 。

Across the country, the number of retirees in many provinces has reached "one million". Beijing, Jiangxi, Inner Mongolia and other places have more than 3 million people, Guangdong has more than 7 million people, and Zhejiang has up to 9.15 million people 。

Previously, a half month talk article said that from now to the next 10 years, China will usher in the largest "retirement tide" in history, The post-60s group continued to enter retirement life, retiring at an average annual rate of 20 million people 。

Since January this year, China has officially implemented the national pooling of pension insurance. As the "first pillar", although the coverage of basic pension is wide, its replacement rate is declining year by year; As the second pillar, the coverage of enterprise annuity and occupational annuity is relatively small.

Not long ago, the "third pillar" of personal pension has come out. How will the new top-level design fill the pension gap? In the face of more and more "new" elderly groups, how to ensure their old age?

The largest "retirement boom"

In 2022, men born in 1962 will reach the retirement age of 60, and most ordinary female workers born in 1972 will also retire this year.

In fact, since 1949, China has experienced three "baby booms" in 1950-1958, 1962-1975 and 1981-1997. The biggest one was the wave peak that began in 1962.

During this period, China's annual average birth population reached 25.83 million, 5.06 million and 3.77 million more than the previous two "baby booms".

It can be inferred that the "post-60s" and "post-70s" born during this peak period will enter the old age period around 2022-2035 and become the "main force" of the retirement tide. according to National Bureau of Statistics Data sorting, In the 1960s, the birth population reached 239 million, and then in the 1970s, it reached nearly 217 million 。

It is worth noting that the population born in 1963 is the highest in the past 70 years, with 29.75 million newborns and a birth rate of 43.60 ‰. This also means that more people may retire next year.

The impact of this round of "retirement boom" will be multifaceted.

First, the working age population continues to decline significantly. Peng Xizhe, director of the Population and Development Policy Research Center of Fudan University and president of the Institute of Aging Research of Fudan University, pointed out that in this wave of "retirement tide", more than 20 million people will retire every year; At the same time, China's annual potential labor supply is about 17 million to 18 million. in other words, China will reduce the working age population by 3 to 5 million every year 。

This will increase pension pressure. Peng Xizhe said that, on the one hand, the number of retirees increased, leading to an increase in the number of pensioners; On the other hand, the number of retirees is more than the number of newly added employees, and the number of pensioners will continue to decline.

Current situation of the two pillars

At this stage, China's multi-level endowment insurance system mainly includes three aspects, namely "three pillars".

The first pillar is basic pension insurance, including pension insurance for urban employees and urban and rural residents. In terms of coverage, more than 90% of the country's population has pension insurance. However, there are still differences in pensions between different sectors.

Ouyang Li is less than 4 months away from "official retirement". What she will focus on is the "basic pension" that most people are familiar with.

Eight years ago, Ouyang Li, who had been doing business for half his life, left his hometown and moved to the provincial capital city with his family, finding a stable job. Originally thought that the social security of urban workers had been paid, and the future pension would be safe.

But when she was about to retire, the staff of her old family's social bureau told her that because she was New City The social insurance payment for less than 10 years does not comply with the local "retirement policy", but also has reached the statutory retirement age. She must return to her hometown this year to handle retirement and "start to receive pension".

Ouyang Li is looking for a solution. She told us, "Although I have paid insurance in the provincial capital for less than 10 years, I can't apply for retirement; but also for less than 15 years, it is said that I can apply for delayed retirement online and continue to pay social insurance at my own expense for several years. With the principle of" more pay, more pay ", I will get more pensions in the future."

In order to fight for the possibility of "more pensions", Ouyang Li is still busy between the two cities.

Although the coverage rate is high, as Wang Zengwen, a professor in the Department of Public Economy and Social Security of Wuhan University, said recently, "the basic pension insurance or basic pension has returned to the level of basic life. If you need a higher standard of living, or a higher security level and a higher level of service, you must pass the other two pillars."

The second pillar besides basic pension is enterprise pension or occupational pension.

Tian Hong, who retired in 2020, had previously worked in a large state-owned enterprise, and the enterprise would pay an "annuity" for him every month. Before retirement, her monthly income was about 6500 yuan; In the past two years since retirement, her monthly basic pension has been about 5300 yuan, but in the first three years of retirement, the enterprise annuity will give her a supplementary pension of about 2800 yuan per month.

As a result, her actual monthly income at the beginning of retirement was about 8100 yuan, nearly 1600 yuan higher than when she worked. "Although the annuity is only returned for three years, it can only be regarded as a transition, and it will not make people's living standards plummet after retirement. But with this money, many colleagues are also looking forward to retirement." Tian Hong said with a smile.

However, people like Tian Hong are still a minority. As Peng Xizhe, director of the Population and Development Policy Research Center of Fudan University, pointed out earlier, as the "second pillar", enterprise annuity and employee annuity have developed to a certain extent in recent years, but the coverage of the population is still limited, and enterprises and public institutions face greater economic burden pressure.

According to the data disclosed by the Ministry of Human Resources and Social Security, by the end of 2021, the number of enterprises that have established annuities nationwide is 117500, with 28.75 million employees participating, with a total scale of about 2.64 trillion yuan. And based on National Bureau of Statistics According to the data, the domestic employed population at the end of the same year was about 746 million. This means that, Only about 3.85% of the employed population nationwide participate in enterprise annuity or employee annuity 。

Build a multi pillar system

As early as 2020, the "14th Five Year Plan" has clearly defined the need to "develop a multi-level and multi pillar endowment insurance system, improve the coverage of enterprise annuities, and standardize the development of the third pillar endowment insurance". 2021 and 2022 the state council In the government work report, it was successively proposed to standardize the development of the third pillar pension insurance.

The so-called third pillar endowment insurance is personal savings endowment insurance and commercial endowment insurance. Previously, there was no national unified institutional arrangement in relevant fields, which was the weakness of the multi-level pension insurance system. In April this year, the state officially issued the Opinions on Promoting the Development of Personal Pension, and the "gap" of the third pillar system was finally filled. The news at the beginning of this month shows that Chengdu has become the leading city of individual pension in Sichuan Province.

This is not a "replacement", but a better "supplement", giving ordinary people more choices.

Hu Jiye, a professor in the Department of Capital Finance at the Business School of China University of Political Science and Law, previously analyzed that the first and second pillars are linked to the unit, while "the introduction of the third pillar actually creates a new space for our in-depth combination of pension and capital market. We have no right to choose in the first pillar and the second pillar. We have the right to choose in the third pillar."

Globally, Japan's iDeCo plan (defined pension with individual contribution), Germany's Liszt plan, and the United States' IRAs (individual retirement accounts) are actually successful representatives of the third pillar. Referring to the experience of Japan, Germany, the United States and other countries, the construction of the third pillar is particularly important for low-income groups and flexible employment groups.

However, even if personal pension is implemented, it may take some time to relieve the pressure of pension. People's Bank of China Yao Yudong, the former director of the Financial Research Institute, believes that to ease the pressure on the pension of the first pillar, the replacement rate of the third pillar should be at least 10%.

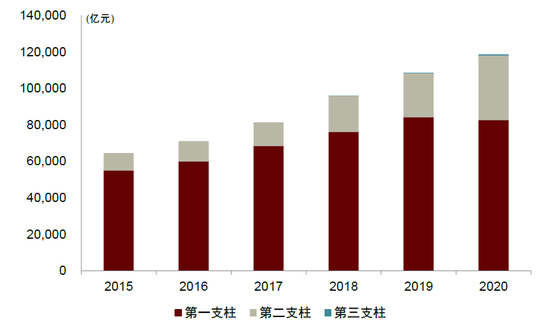

The first pillar of the pension system in China has a large scale Source: Zhongjin Touching the Eyes

The first pillar of the pension system in China has a large scale Source: Zhongjin Touching the Eyes Therefore, the country is still "strengthening" one or two pillars.

For the first pillar, since its establishment in the 1990s, China's old-age insurance system has been gradually improving the level of overall planning from the county level. In July 2018, China established and implemented the central fund adjustment system, which appropriately balanced the burden of pension insurance funds between provinces. Since January of this year, China's pension insurance has further started to implement national planning.

For the second pillar, in January 2021, the state also issued the Notice on Adjusting the Investment Scope of Annuity Fund to address the shortcomings of enterprise annuities and occupational annuities, making adjustments to the investment scope of annuity fund, including increasing the proportion of equity investment from 30% to 40%.

When the retirement tide comes, the old people are trying to attach more layers of "insurance" to the "purse" of their old age.

(The interviewee in the article, Ou Yangli, is a pseudonym)

Journalists| Huang Mingyang

Massive information, accurate interpretation, all in Sina Finance APP

Editor in charge: Li Moxuan