Opinion Leader | Lee Xianglong

►►► Core viewpoints

On May 17, the yield of 10-year treasury bonds returned to around 2.30% again, and the bond market has been in a wide range of shocks recently. The phenomenon of long short game is serious.

There are both positive and negative factors in the bond market. For the positive factors, first, the financial data of April was lower than the market expectation. In the weekly report last week, we pointed out that: on May 11, the central bank announced the financial data of April, and it was rare for M1 to show a negative increase on a year-on-year basis and new social financing at the same time, reflecting that credit easing still needs policy development; Second, the scale of wealth management increased sharply in April. The scale of wealth management in April 2024 increased by about 2.95 trillion yuan month on month to 29.28 trillion yuan, far exceeding the average of 1.87 trillion yuan in April 2018-2023, and significantly exceeding market expectations. Behind the larger than expected growth of wealth management scale is the deposit interest rate reduction and the central bank's strict investigation of the chaos of "manual interest compensation", which has promoted the transfer of deposits to wealth management. This phenomenon may continue to promote the bond market against the backdrop of the current asset shortage.

As for the bad news in the bond market, the first is the supply of interest rate bonds, especially the issue of special bonds, which is also the bad news factor that investors were most concerned about previously. However, from the arrangement for the issuance of 2024 ultra long term special bonds announced by the Ministry of Finance on May 13, the issuance cycle of this year's 1 trillion ultra long term special bonds is longer than the market expectation, and the issuance rhythm is relatively slow, It is conducive to avoiding the periodic pressure on the capital surface caused by centralized issuance, so this factor can be said to be all bad. Second, the real estate policy and the recovery of economic fundamentals driven by it.

In fact, the current analysis logic of the bond market is quite different from that in the past (for example, MLF interest rate is also difficult to become the anchor of the yield of 10-year treasury bonds). In the context of the central bank's easing expectations and the tortuous recovery of the economy in the early stage, the runaway market under bond market transactions has dominated. We believe that, If there is a major correction in the current bond market, it is more affected by the financial supply and the degree of capital easing. The bond market may be "passive" to the economic fundamentals. In the future, it is still possible to cut reserve requirements and interest rates, which will have more friendly effects on the bond market. In addition, although the real estate policy also has negative effects on the bond market, the effect of policy implementation needs to be observed in the short term.

Therefore, for the bond market in June, we maintain the judgment in the report "April's financial data is less than expected, short-term is favorable for the bond market or again": At present, the bond market may move back from shock to strong shock. However, against the backdrop of the central bank's repeated statements on the yield of long-term bonds, it is difficult to decline too much in the short term. Under the condition that the subsequent capital is still loose, the steep market may still exist. If appropriate, you can make long and short bonds. For the long end, the callback or the buying time point is still.

Overall:

Based on the above, we will Great Wall Securities The bond portfolio is set as follows: 40% of the bullet type 3-year national bonds and 60% of the 3-year AA corporate bonds are allocated without leverage.

1 Current macro-economy and enterprise environment

Macroeconomic environment: offline tourism consumption is hot, and real estate is still sluggish

According to the May Day consumption data, offline tourism consumption is relatively hot, and it is generally in the stage of volume increase and price decrease. On May 6, according to the data center of the Ministry of Culture and Tourism, the total number of domestic tourism trips nationwide was 295 million, up 7.6% year on year, and 28.2% on a comparable basis compared with the same period in 2019; Domestic tourists spent 166.89 billion yuan on travel, up 12.7% year on year and 13.5% on a comparable basis compared with the same period in 2019. Although per capita spending has slightly contracted compared with 2019.

However, on May 17, the National Bureau of Statistics released relevant data on real estate investment sales. From January to April, the sales growth rate of new commercial housing nationwide was - 28.3%, which was expanded again after the decline narrowed from January to March. The growth rate of real estate development investment nationwide was - 9.8%, and the decline continued to expand. It can be seen that the current consumption of residents is generally "small" consumption such as offline tourism, while "large" consumption such as real estate is still lack of motivation.

In addition, on May 11, the Central Bank also released the financial data of April. In the data, social finance increased by 19.87 billion yuan in a single month in April, an increase of 1.42 trillion yuan less than the previous year. The growth rate of social finance stock fell to 8.30% year on year. In April, M1 increased by - 1.4% year on year, a decline of 2.5 percentage points month on month. The M2-M1 scissors spread expanded to 8.60%, indicating that the index (M2-M1)/M1 of the trend of deposit periodization also continued to hit a new high. We also pointed out in the previous report, "April's financial data is less than expected, which may be favorable for the bond market again in the short term", M1 and new social financing are negative at the same time, which is rare in history, reflecting the need for policies to expand credit. It is more favorable to the bond market in the short term.

Macro policy environment: the Political Bureau meeting in April laid the policy keynote, and various heavy policies on real estate were introduced in May.

The meeting of the Political Bureau of the CPC Central Committee in April continued to emphasize the general tone of economic work of "seeking progress while maintaining stability", and recognized the "good start" of the current economy. It pointed out that "the number of positive factors in the economic operation has increased, the driving force has continued to increase, social expectations have improved, high-quality development has been solidly promoted, showing the characteristics of rapid growth, structural optimization, good quality and efficiency, and the economy has made a good start". But at the same time, it also pointed out that many challenges faced by the sustained recovery of the economy are mainly that effective demand is still insufficient, enterprises are under great pressure to operate, there are many risks and hidden dangers in key areas, the domestic big cycle is not smooth enough, and the complexity, severity and uncertainty of the external environment are rising significantly ". The overall judgment on the domestic and foreign economic environment is basically consistent with the Central Economic Work Conference held in December last year.

In addition, the meeting of the Political Bureau also highlighted the importance of real estate, "We should take into account the new changes in the relationship between supply and demand in the real estate market and the new expectations of the people for high-quality housing, and comprehensively study the policies and measures to digest the stock of real estate and optimize the incremental housing".

Therefore, since May, various heavy real estate policies have been introduced in succession. First, in the evening of May 6, Shenzhen further optimized its real estate policies, which mentioned that seven regions, including Yantian District, Bao'an District (excluding Xin'an Street and Xixiang Street) and Longgang District, have relaxed purchase restrictions, and the payment period of individual income tax and social insurance for property buyers has been adjusted from three years to one year, Shenzhen registered resident families with two or more minor children can purchase another house in the above areas. Secondly, on May 9, purchase restrictions were completely lifted in Hangzhou and Xi'an.

Finally, on May 17, the People's Bank of China issued four heavy policies for real estate First, set up 300 billion yuan of affordable housing refinancing. Encourage and guide financial institutions to support local state-owned enterprises to purchase the completed but unsold commercial housing at a reasonable price and use it as affordable housing for rationing or leasing in accordance with the principles of marketization and rule of law. The second is to reduce the minimum down payment ratio of individual housing loans at the national level, and adjust the minimum down payment ratio of the first house from 20% to 15%, and the minimum down payment ratio of the second house from 30% to 25%. Third, the lower limit of the national individual housing loan interest rate policy was abolished. The loan interest rate for the first and second homes will no longer set a policy floor, so as to realize the marketization of housing loan interest rate. Fourth, the interest rate of housing provident fund loans of various maturity categories was lowered by 0.25 percentage points. After the adjustment, the loan interest rate of personal housing provident fund for the first housing for more than five years is 2.85%, which can better meet the housing needs of the depositors of housing provident fund.

We believe that the current real estate data continues to decline, and various policies have been issued in full swing. At present, the provinces or cities in China still retain housing purchase restrictions. In addition to Beijing, Shanghai, Guangzhou, and Shenzhen, the four first tier cities, Hainan Province and Tianjin are still in the state of partially liberalizing purchase restrictions, and relevant measures may follow. However, due to the obvious contraction of the current residents' balance sheet, it remains to be seen whether the policy can bring about actual effects in the short term.

Bank funds: Reverse repo has been operated for a long time in recent two months, but the market is not "short of money"

In April, the central bank released 652 billion yuan of currency through open market operations, and withdrew 1202 billion yuan of currency, far more than the release, with a net withdrawal of - 550 billion yuan. As of May 14, the central bank released 16 billion yuan of currency through open market operations.

We have pointed out in several reports in April that the current market is not "short of money", and even has abundant funds R007 It also fluctuated almost all the time within 20BP above the policy interest rate (OMO interest rate, 1.8%), which was at a level more desirable to the central bank. Therefore, the reverse repo of the central bank in the past two months was a "volume" operation (2 billion yuan was put in every day).

In terms of capital interest rate, as of May 14, the weighted interest rate (DR007) of pledge style repo of 7-day deposit institutions was 1.84%, a decrease of 3BP from 1.87% on April 1. In fact, from April to May 14, DR007 exceeded 2.0% on April 29 and 30, and all others were in the range of 1.8% - 2.0%. The weighted interest rate (R007) of 7-day inter-bank pledge repo was 1.84%, which was significantly lower than 2.14% on April 1. If you look at the monthly average, DR007 was 1.88% and R007 was 1.96% in April. As of May 14, the monthly average DR007 was 1.85% and R007 was 1.88, both of which declined.

Enterprise profit and financing environment: the growth rate of enterprise profit slows down, and the financing environment is differentiated

We pointed out in the early report "Will the bond bull market continue after the two sessions?" that from January to December 2023, although the profit of industrial enterprises above the designated size in China is still negative, the decline is narrowing, and then superimposed on the low base in the same period, the profit of subsequent enterprises is more likely to repair year on year, It can be seen from the current published cumulative year-on-year profit figures of industrial enterprises above designated size nationwide (10.2% in January February 2024, 4.3% in January March 2024), It is true that this year has turned from negative to positive, but the value from January to March is significantly lower than that from January to February, indicating that the current economic recovery is still slow and tortuous.

From the perspective of financing environment, corporate financing is differentiated, credit financing is good, and direct financing is poor. The financial statistics for April released a few days ago showed that in April, corporate loans increased by 860 billion yuan in the same month, an increase of 176.1 billion yuan over the same period last year, which is a good figure. Although short-term loans increased by - 410 billion yuan in the same month, medium and long-term loans increased by 4100 yuan in the same month, and bill financing was 834.1 billion yuan, which offset the decline of short-term loans. In addition, in terms of direct financing in social financing data, in April, bond financing increased to 49.3 billion yuan in the same month, an increase of 244.7 billion yuan less than the same period last year, and equity financing increased to 18.6 billion yuan in the same month, an increase of 80.7 billion yuan less than the same period last year. Direct financing is poor.

2 Interest rate market analysis

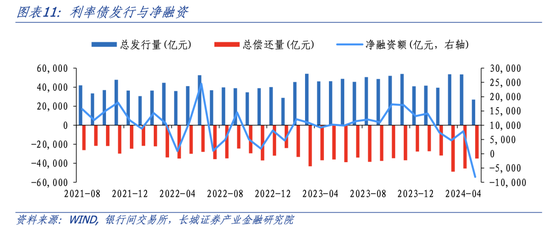

Primary market: net financing rose month on month in April and May, and issuance costs continued to decline

In April, the total issuance of interest rate bonds, including government bonds, local government bonds, financial bonds and inter-bank deposit certificates, was 5345 billion yuan, the total repayment was 4558.9 billion yuan, and the net financing was 786.2 billion yuan, up from March (468.8 billion yuan in March), but down from the same period last year. As of May 14, the total issuance was 2687.5 billion yuan. It is estimated that there will still be about 5-5.5 trillion yuan in the whole month. However, the total repayment in May was 3498.8 billion yuan, significantly lower than that in March and April, Therefore, the month on month net financing volume in May is expected to continue to be higher than that in April. It can be seen that the net financing amount of interest rate debt, which has remained depressed since February, may have an upward trend in the follow-up.

In terms of issuing interest rate, as of May 14, the nominal interest rate of treasury bonds, local government bonds, policy bank bonds, and interbank deposit certificates was 1.85%/2.47%/2.13%/2.03%, respectively. Among them, treasury bonds, policy bank bonds, and interbank deposit certificates decreased by 2BP/1BP/4BP compared with April, and local government bonds increased by 6BP compared with April, which shows some differentiation. However, compared with the same period last year, the four items decreased by 34BP/38BP/46BP/38BP respectively.

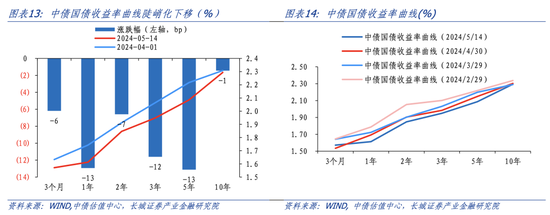

Secondary market: steep downward shift of yield curve

From April to May 14, the yield curve of Chinese government bonds showed a steep downward trend. Among the long-term interest rates, the yield of 10-year government bonds fell from 2.31% on April 1 to 2.29% on May 14. Although the decline was not deep, it actually fluctuated widely. The yield of 5/3/2/1-year treasury bonds decreased by 13BP/12BP/7BP/13BP to 2.09%/1.95%/1.85%/1.61% from the beginning of April. As we mentioned earlier, At present, although the central bank has been taking the "land volume" operation of 2 billion yuan per day in reverse repurchase, the market is not short of money, and the economy is still recovering twists and turns (good export data, poor financial data, and low real estate). Short end interest rates and long-term interest rates have both moved down, with a greater decline in the short end.

From April to May 14, although the yield of 10-year treasury bonds has only declined by 2BP as a whole, it is in a wide range of fluctuations, and once fell to the lowest point of 2.22%. Looking back at the whole path, we can see that in early April, the yield of 10-year treasury bonds remained volatile around 2.3%. As the inflation data for March released by the Bureau of Statistics on April 11 was lower than expected, the yield fell in response, and then superimposed the "asset shortage" and other factors, it reached the lowest point of 2.22% on April 23. Then on the same day, the head of the relevant department of the Central Bank warned that the yield of long-term bonds was too low, "The yield of long-term treasury bonds will always run within a reasonable range matching the long-term economic growth expectations". The yield rose sharply in the following days, and returned to 2.35% at the highest on the 29th. At the beginning of May, as the market calmed down and the monetary fundamentals were relaxed, the yield returned to around 2.30% again and remained volatile, only rising to 2.33%. On May 11, the central bank announced financial data for April that was less than expected, M1 has a negative increase year on year and social finance, and the bond market has moved from shock to strong shock. However, various real estate related policies and rumors announced in mid May still have a disturbance to the bond market.

The trend of CDB bonds is basically the same as that of national debt, but since April, CDB bonds have been in a state of wide range shock and strong The yield declined slightly from 2.41% on April 1 to 2.36% on May 14, a decrease of 5BP. The overall downward trend of the yield is greater than that of national debt (national debt declined by 2BP). The ratio of CDB bonds to government bonds also declined, from 1.05 to 1.03.

According to the published situation of interest rate bonds held by institutions in March 2024, Most commercial banks, credit cooperatives, insurance institutions and securities companies are increasing their holdings of interest rate bonds. In terms of the specific situation of branches, commercial banks are significantly increasing their holdings of government bonds and local government bonds, as well as financial bonds and interbank certificates of deposit; Credit cooperatives are increasing their holdings of government bonds, local government bonds, and financial bonds, but reducing their holdings of interbank certificates of deposit; Insurance institutions are increasing their holdings of treasury bonds, local government bonds and financial bonds, but also reducing their holdings of interbank certificates of deposit; Securities companies only increased their holdings of financial bonds, but reduced their holdings of government bonds, local government bonds, and interbank certificates of deposit.

3 Credit market analysis

Primary market: the net financing amount declined month on month, and the issuance interest rate continued to decline

Issuance and net financing: In April, the total issuance scale of credit bonds, including short-term financing, medium-term notes, corporate bonds, corporate bonds and directional instruments, was 1400.8 billion yuan, lower than that in March but unchanged from the same period last year; The total repayment amount was 1213.1 billion yuan, and the net financing amount was 187.7 billion yuan, lower than last month but higher than the same period last year. As of May 14, the total issuance scale of credit bonds was 293.8 billion yuan, a low value (half of the time has passed). The total repayment in May was 677.3 billion yuan, so Even if the overall net financing in May is positive, the value is difficult to be higher 。

In terms of issuing interest rate: From the monthly weighted average coupon rate of credit bonds issued in the primary market (weighted by the actual total issuance of corporate bonds, corporate bonds, medium note interest rates and short-term financing interest rates), the interest rate of credit bonds in April was 2.50%, down again from 2.64% in March, and 2.38% as of May 14th, down again on the basis of April At present, the downward trend of monthly weighted average coupon rate of credit bonds is still 。 Specifically, in April, the interest rates of corporate bonds, corporate bonds, medium-term notes and short-term financing were 2.67%/2.78%/2.83%/2.05%, respectively, down 17BP/27BP/10BP/18BP from March. As of May 14, the issuing interest rates of corporate bonds, corporate bonds, medium notes and short-term financing were 2.72%/2.80%/2.75%/1.94%, respectively. Corporate bonds and corporate bonds increased by 5BP and 1BP, while medium notes and short-term financing decreased by 9BP and 11BP. The decline in the nominal interest rate of corporate bonds and corporate bonds has been curbed.

Secondary market: steep downward trend in yield, AAA credit spread generally narrowed

The yield of AAA rated credit bonds with different maturities has declined sharply As of May 14, the yield of six month/one year/three year/five year/ten year varieties had declined 27BP/25BP/18BP/21BP/9BP to 2.06%/2.11%/2.32%/2.45%/2.67% respectively from the beginning of April, and the decline of short-term interest rate was higher than that of long-term interest rate.

Credit spread As of May 14, the AAA credit spreads were shrinking compared with the beginning of April, and the six month/one year/three year/five year/ten year varieties were reduced by 19BP/12P/7BP/8BP/8BP/8BP respectively.

In the AA/AAA grade interest margin, the six-month/one-year period remained unchanged, and the three-year/five-year/10-year period decreased by 7BP/5BP/15BP respectively.

Real estate bonds: the issuance decreased month on month, and the net financing remained negative

Real estate financing The total issuance in April was 49.377 billion yuan, a significant decrease compared with March (56.196 billion yuan in March), but currently it is the second highest in this year, with a total repayment of 51.227 billion yuan, so the net financing was 1.85 billion yuan. As of May 14, the total issuance was only 4.33 billion yuan, so the total monthly issuance is not expected to be very high, while the total monthly repayment in May was 31.9 billion yuan, It is estimated that the overall net financing amount in May is still negative. It can be seen that the current real estate financing is still not ideal. At present, the transaction area of commercial housing in 30 large and medium-sized cities is still low, and it is still the lowest value in recent five years from the data.

Urban investment bonds: the decline of net financing scale expanded in April, and may narrow in May

In April, the total issuance of urban investment bonds was 362.1 billion yuan, a month on month decline, and significantly lower than the same period last year (525.7 billion yuan). The total repayment was 471.5 billion yuan, so the net financing amount was -109.3 billion yuan, a new low since this year. In addition, as of May 14, the total circulation was 74 billion yuan, and it is estimated that the total circulation in the whole month would hardly exceed 200 billion yuan, but the overall total repayment in May was 238.4 billion yuan, Therefore, from the perspective of net financing, the month on month ratio in May may be narrowed.

4 Great Wall Securities Bond Investment Index

Last month review

As of May 17, the bond investment index of Great Wall Securities was 103.02 (100 on January 2, 2024), which continued to rise from the beginning of April (102.44 on April 1). In addition, the China Bond New Comprehensive Wealth (Gross Value) Index (CBA00101. CS) is 102.59, and the China Bond Total Price Index (CBA00303. CS) is 101.46, both below our index.

June Strategy

On May 17, the yield of 10-year treasury bonds returned to around 2.30% again, and the bond market has been in a wide range of shocks recently. The phenomenon of long short game is serious.

There are many factors in the bond market. For the positive factors, first, the financial data in April was lower than the market expectation, In the weekly report last week, we have pointed out that: on May 11, the central bank released the financial data of April, and it is rare for M1 to have negative growth on a year-on-year basis and new social financing at the same time, which shows that credit easing still needs policy efforts; Second, the financial management scale increased sharply in April In April 2024, the scale of wealth management increased by about 2.95 trillion yuan month on month to 29.28 trillion yuan, far exceeding the average of 1.87 trillion yuan in April 2018-2023, and significantly exceeding market expectations. Behind the larger than expected growth of wealth management scale is the deposit interest rate cut and the central bank's strict inspection of manual interest supplement, which has promoted the transfer of deposits to wealth management. This phenomenon will continue to play a role in promoting the bond market in the context of the current asset shortage.

For the bad news in the bond market, first is the supply of interest rate bonds, In particular, the issue of special treasury bonds, which was also a negative factor that investors had previously been most concerned about, but from the arrangement for the issuance of ultra long term special treasury bonds in 2024 announced by the Ministry of Finance on May 13, the issuance cycle of this year's 1 trillion ultra long term special treasury bonds is longer than the market expectation, and the issuance rhythm is relatively gentle, which is conducive to avoiding phased pressure on the capital surface due to centralized issuance, Therefore, this factor can be said to be the best of the bad. Second, the real estate policy and the recovery of economic fundamentals driven by it (The previous article has emphasized that the central bank issued a number of policies to boost the real estate in the case of the real estate data continuing to decline in April).

In fact, the current analysis logic of the bond market is quite different from that in the past (for example, MLF interest rate is also difficult to become the anchor of the yield of 10-year treasury bonds). In the context of the central bank's easing expectations and the tortuous recovery of the economy in the early stage, the runaway market under bond market transactions has dominated. We believe that, If there is a major correction in the current bond market, it is more affected by the financial supply and the degree of easing of funds. However, the bond market may be somewhat "passive" to the economic fundamentals. In the future, it is still possible to cut reserve requirements and interest rates, which is more friendly to the bond market. In addition, although the real estate policy has negative effects on the bond market, the effect of policy implementation needs to be observed in the short term( This is why after the central bank announced four heavy real estate policies on the morning of May 17, the bond market corrected, but in the afternoon, the bond market rose again, behind which was the logic that all the bad things went out and the bond market continued to rise )。

Therefore, for the bond market in June, we maintain the judgment in the report "April's financial data is less than expected, short-term is favorable for the bond market or again": At present, the bond market may move back from shock to strong shock, but in the context of the central bank's repeated "guidance" on long-term bond yields, it is difficult to go too far down in the short term. Under the condition that the subsequent capital is still loose, the steep market may still exist. If appropriate, you can make long and short bonds. For the long end, the callback or the buying time point is still.

population

Based on the above, we set the bond portfolio of Great Wall Securities in June as: 40% of the bullet type 3-year national bonds and 60% of the 3-year AA corporate bonds are allocated, without leverage.

Risk warning

Domestic macroeconomic policies are not as expected; Monetary policy is not as expected; Real estate policy exceeded expectations; Fiscal policy exceeds expectations; Credit events broke out intensively.

Source: CGWS fixed income research

(The author of this article introduces: the head of the fixed income team of the Great Wall Securities Industry Finance Research Institute, responsible for finance, finance, and interest rate debt research.)